I truly believe that longevity biotechnology can save America.*

I just came back from DC, where I spoke to congress as part of the Alliance for Longevity Initiatives. They put together a rare bi-partisan call for action. We need the government to recognize just how impactful longevity can be on our country’s biggest problems.

We are facing:

- Exploding government debt and deficits

- Social security going bankrupt

- Growing medical care/insurance costs

- Slower GDP growth

- Lower fertility rates

Many policymakers blame America’s aging population for these problems. But living longer isn’t the problem – getting old is. Keeping people young, healthy and productive can genuinely address these challenges.

This is what we told congress. We want to share it with you, so this movement can keep growing.

*Longevity can save many other countries too

How Longevity Reduces Debt and Deficits:

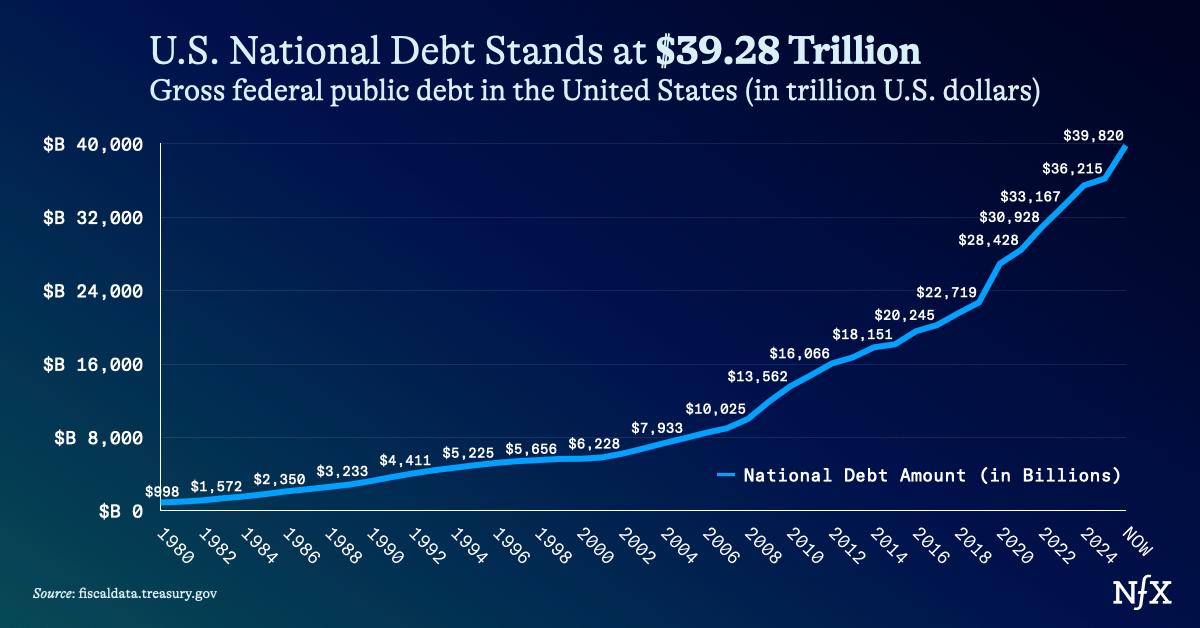

You’ve likely seen this national debt graph:

And, you’ve seen our growing deficits – how much more the government spends versus earns each year. The national debt as of June 2026 stands at $39.28T, and is growing.

Most of the reason we spend more than we make comes down to exploding non-discretionary spending on Medicare, Medicaid, Social Security, and interest payments on our high national debt.

Longevity tackles all these major problems:

Young and healthy people spend far less on healthcare than older people. Adults aged 65 and older are 18% of the population, but they account for 36% of healthcare spending – their share of healthcare spending is twice their share of the population.

We see the opposite effect in younger populations. The younger cohorts of 19-34 make up only 21% of the population, and spend 12% on healthcare – their share of healthcare spending is about half of their share of the population.

Longevity technology is about keeping people as healthy at 65 as they are at 19.

It may seem like an “out there” approach, but it’s not. We have the technology to keep people’s bodies younger and healthier. In the long run, we are already spending this money treating people when they get sick.

Why not spend it now on keeping them healthy?

The question isn’t whether we can extend human life and healthspan anymore. It’s whether we can afford not to.

Now, let’s tackle the second piece: retirement spending, pensions, and social security. Spending on these programs is projected to outpace revenues, primarily due to the aging baby boomer population. But there are other reasons this system may break down in the future if we keep on this track.

The idea of a social security safety net became prominent during the Industrial Revolution, but in the US, formal state-backed pension systems began during the Depression Era. The US Social Security Act sets the “retirement” age in your mid-sixties. But at that time, a person’s life expectancy was actually around 60 years old. The gap between retirement and death was minimal at best—the system was designed assuming most people would work until they died or very close to it.

Today, humans live about 15-20 years longer, but we haven’t proportionally increased our healthspan—the number of healthy, productive years we have. This creates two problems:

- Extended dependency period: We’re drawing on Social Security and Medicare for 15-20 years instead of 2-5 years.

- Accelerated healthcare costs: We’re getting progressively sicker during those extended years, requiring more expensive medical interventions.

The current retirement system assumes people become unproductive in their 60s and require 15-20 years of financial support. If 70-year-olds had the capabilities of today’s 30-year-olds, they could continue contributing to the economy, paying taxes, and building wealth instead of drawing down savings and social benefits.

Today, the largest cohort of savers and investors in our society consists of people aged 50-65 who have finished paying off their mortgages, no longer support children, and are at peak earning potential. These cohorts tend to earn more than they consume. We could extend that period out by decades, allowing people to build greater wealth during peak earning years, while their expenses are relatively low, compared to other life stages.

This pays dividends for both society and the individual. A longer life, with a diversity of life stages, is inherently more fulfilling – people could go back to school, take on a second or even third career, and continue to build their own wealth far after the expenses of early life are over.

And, a longer wealth accumulation phase for individuals will have a capital formation effect throughout the whole economy. You can think of financial assets or investment vehicles as ways to shift consumption from one life stage to another. You invest money at 50, and plan to spend that money, plus interest, at 75. You’ve transferred that consumption to 15 years in the future.

In the meantime, that money flows into the economy, reducing the cost of capital. When you have millions more people with more wealth and more time to invest you get:

- Money flowing into bonds, stocks, and other investments

- Pension and retirement funds growing larger

- Institutional investors with more capital to deploy

- Banks with more deposits to lend

- Lower interest rates

Overall, this environment means lower interest rate payments on our national debt (in 2025, those payments were $1.22 trillion – for the first time, higher than defense spending).

A healthier, more productive society is richer, too. We save more, lend more, invest more.

How Longevity Will Increase GDP Growth

So far, we’ve mostly talked about saving money. But longevity will also help America make money. Our GDP growth has stalled, and longevity can reignite it.

First, investing in longevity itself is likely to generate far greater returns than the current “sick care” paradigm we’re living in.

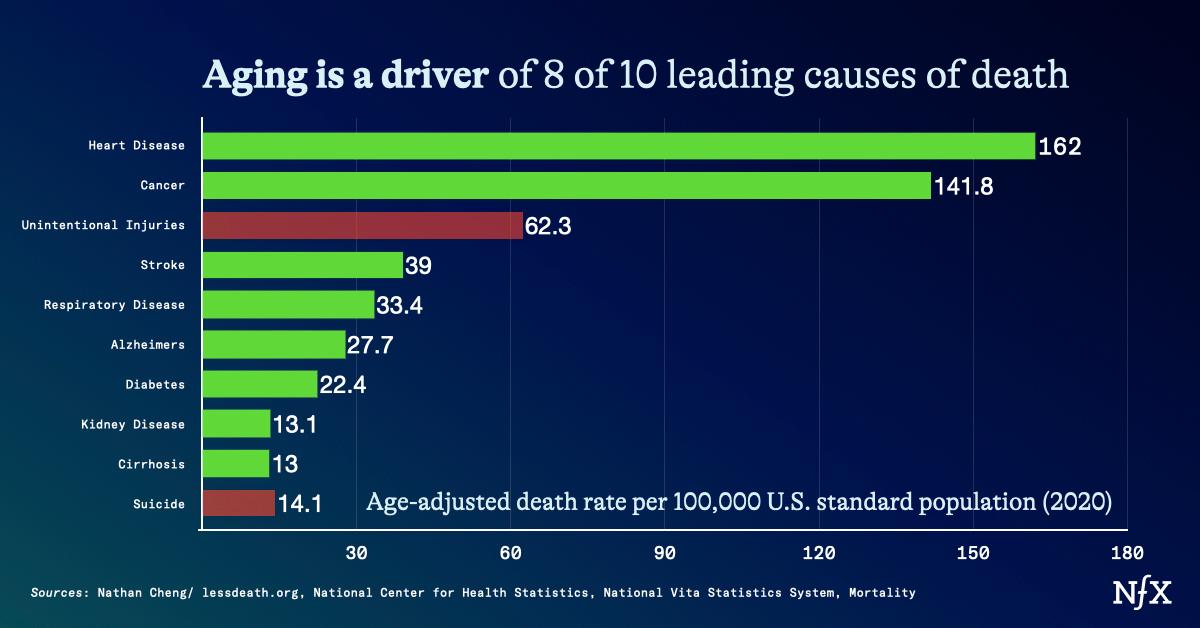

Eight of the ten leading causes of death in the US are manifestations of the same underlying process: biological aging. Longevity research targets aging itself—the root cause underlying most of what kills and disables us.

Taking this approach has been shown to generate greater economic value than addressing each disease individually. That’s because targeting the underlying causes also prevents many of the side effects of disease and aging: loneliness, depression, and limited mobility.

Slowing down aging enough to raise life expectancy by just one year is worth $38 trillion to the United States alone. 10 years is worth $367 trillion.

Second, the economic multiplier effects extend far beyond the direct health benefits. When we extend productive working years, we fundamentally restructure the economy’s growth engine.

Longevity doesn’t just add workers—it also retains our most experienced and productive workers during their peak years of contribution. Currently, we force people out of the workforce precisely when their accumulated knowledge, professional networks, and institutional expertise are most valuable.

Consider the economic impact: if people remain healthy and productive until 85 instead of retiring at 65, we’re adding 20 years of peak-productivity work from people who have spent decades accumulating human capital.

The complementary effects of extended productive careers, reduced healthcare spending, greater consumer spending, greater tax revenue, and reduced caregiver burden all add up.

A recent paper estimated that a single year of life expectancy improvement generates economic value equal to 4-5% of annual GDP—and this benefit repeats every year.

That’s like adding a permanent 4-5% boost to economic growth on top of whatever growth we’d normally achieve. The U.S. economy typically grows 2-4% annually, and longevity could double our normal GDP growth rate.

How Longevity Addresses Fertility Rate

By 2100, more than three-quarters of countries will not have high enough fertility rates to sustain population size. In the US, the fertility rate hit a historic low in 2024.

The real root of this change is that culture has changed faster than biology. We are never going back to a world where there’s no family planning, and families have 10 kids. People now need advanced education, want financial stability, and face housing costs that make starting a family feel prohibitively hard in their mid-twenties. Meanwhile, women’s peak fertility years (20s-early 30s) conflict with career-building years.

We need to adapt our biology to meet this new reality. We need to extend the biological clock to allow people more autonomy over when they can choose to start a family. Imagine if people stayed younger, not just in their health, but also in their ability to have kids much later in life.

This is actually a core focus of longevity research today. Researchers are developing multiple approaches: creating genetically matched eggs from stem cells, improving egg preservation and quality, and extending ovarian function.

To raise the fertility rate, we have to create the right conditions for people to have families on their terms. Longevity is about giving people the opportunity and resources they need.

How To Let Longevity Save America

We can continue down the current path—spending more to manage the consequences of biological aging while our population grows older and more dependent. Or we can make a different choice: invest in longevity as the foundation of 21st-century healthcare.

The first path leads to fiscal crisis, economic stagnation, and social conflict as working-age Americans struggle to support growing numbers of dependent older adults.

The second path leads to economic growth, social vitality, and global competitive advantage.

The choice seems obvious. The question is whether we’ll make it before it’s too late. So what do we need to let longevity save America?

Four things:

Government investment: We need significant federal funding for longevity research at the NIH, FDA , ARPA-H for aging-targeted therapies, and Medicare coverage for proven longevity interventions.

Private capital: Venture capital, private equity, and corporate R&D must recognize longevity as one of the highest-return investment opportunities available today. Billionaires, we’re looking at you.

Regulatory adaptation: Our healthcare regulatory system must evolve to evaluate and approve treatments that target aging processes rather than just specific diseases.

Social infrastructure: We need educational systems that support lifelong learning, employment policies that accommodate longer working lives, and community designs that support healthy aging. It’s how we use longevity to strengthen our economy for the long haul.

Great scientist founders with vision: You have to be thinking seriously big. About how we can get humans to live beyond 160 healthfully. Only then will we make real progress. If you are one of these people, we want to fund you. Talk to us.

The economic case for longevity is overwhelming. The social benefits are undeniable.

Now we just need the will to act.

As Founders ourselves, we respect your time. That’s why we built BriefLink, a new software tool that minimizes the upfront time of getting the VC meeting. Simply tell us about your company in 9 easy questions, and you’ll hear from us if it’s a fit.