Software used to be the hard thing about startups. Now software is easier, and networks are hard. The rare skill today is network bonding.

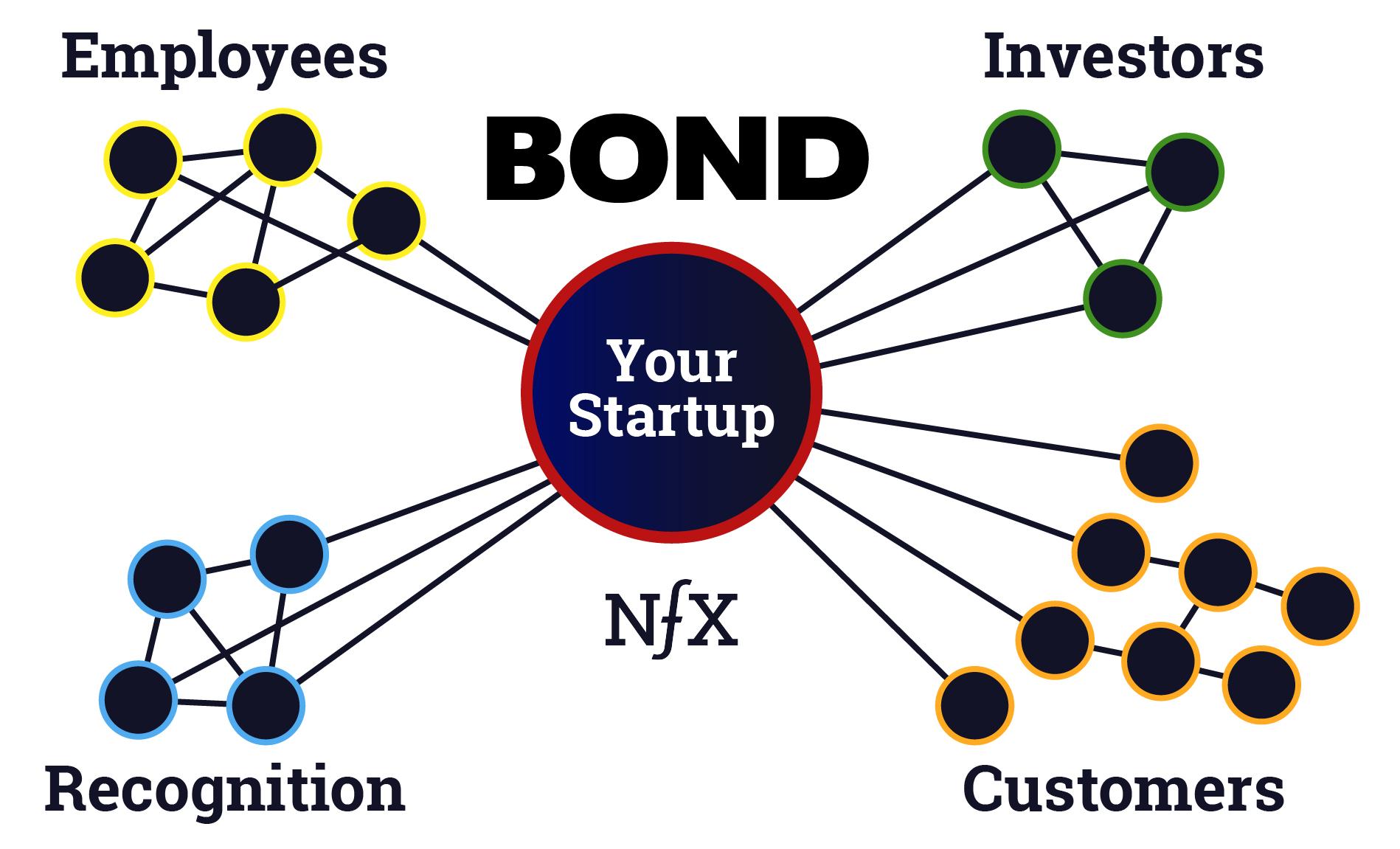

Realize that your startup itself is a network. Your goal is to bond people to it. All kinds of people. When you attach, or bond, one node to your network, it adds value to all the other nodes.

This core idea of “bonding” can be a generalized mechanism applied to how we build all network effects. In this essay, I want to show you a set of mechanisms — which we call Network Bonding Theory — that will help you build startups even better.

Your Startup is a Network, and Has Network Effects

As we’ve said many times, the product of your startup should be a direct network, market network, marketplace network, platform network, etc so it can produce network effects among your users/customers.

But take the next step to realize your startup itself IS a network. Your goal is to attach — and bond — people to your network. Bonding one node adds value to the other nodes. Different nodes bring different value. An investor invests, that gives more value to the VP Marketing you’re trying to hire. When that VP joins, journalists are more likely to bond to your startup by spending their reputation on writing about you and giving you attention. The more attention you get, the easier it is to bond customers to your product. And they all benefit through association with your startup. Classic network effect.

Here’s the thing. Every person or asset you bring to a startup network is bonding to that network in an implicit mathematical equation. They have other options with what to do with their time/money/expertise and they are “getting paid” to bond to your network over other networks. Perhaps they are getting paid in multiple ways, but believe me, there is math underneath it all.

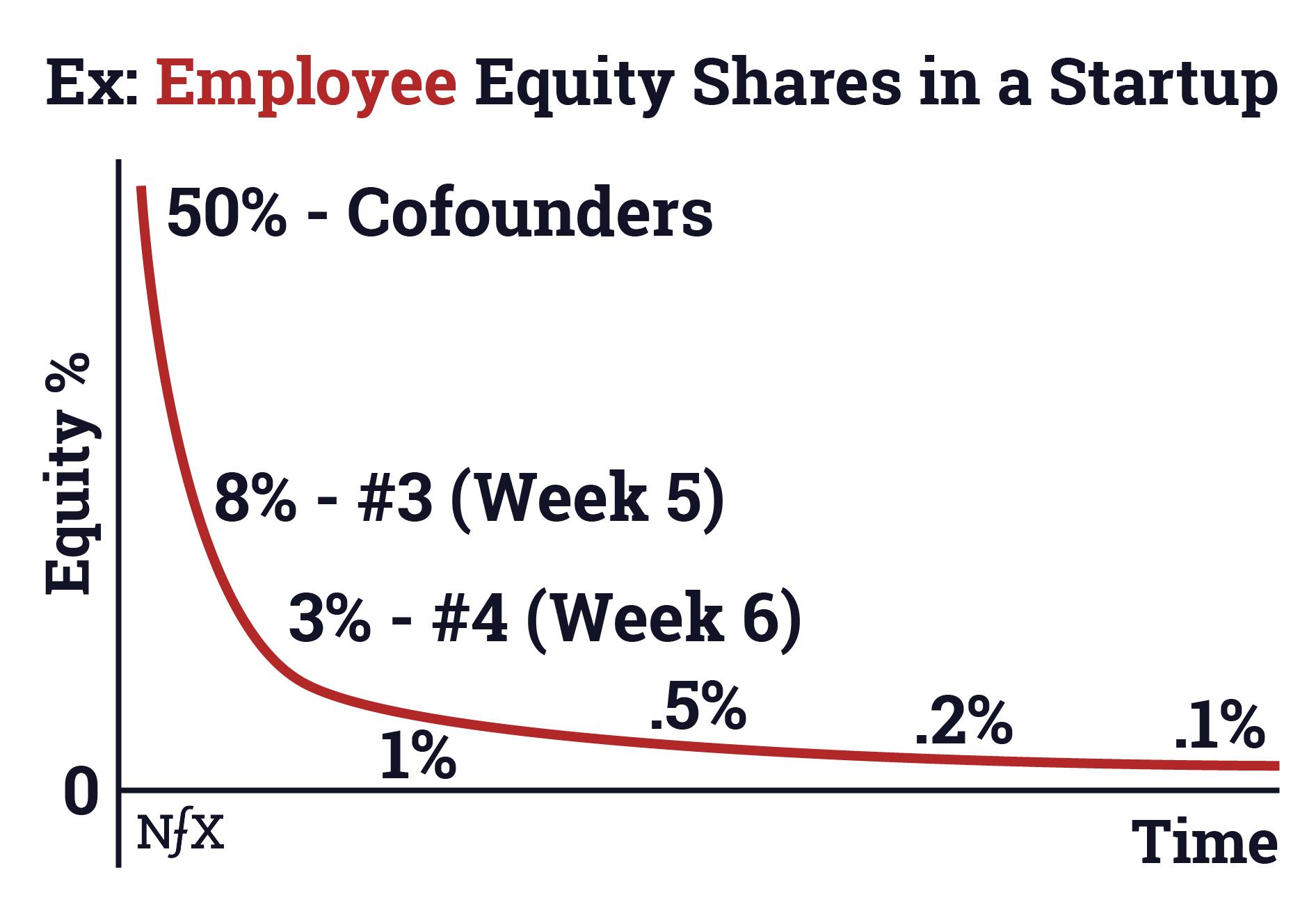

Specifically, let’s take a look at the shares in your startup. Below is a simplified network bonding curve for how much equity your startup needs to pay teammates to join over time. As the strength of your startup gets stronger over time, you have to pay employees less to bond to it. There is more value in the growing network — including less risk — for the employees.

You’ve experienced this yourself. You never called it a “network bonding curve” but it was implicitly there. In the future this will become more explicit, measured and standardized. Network Bonding Theory will become as discussed and as visible to startups from day one as things like Product Market Fit and 1000 True Fans.

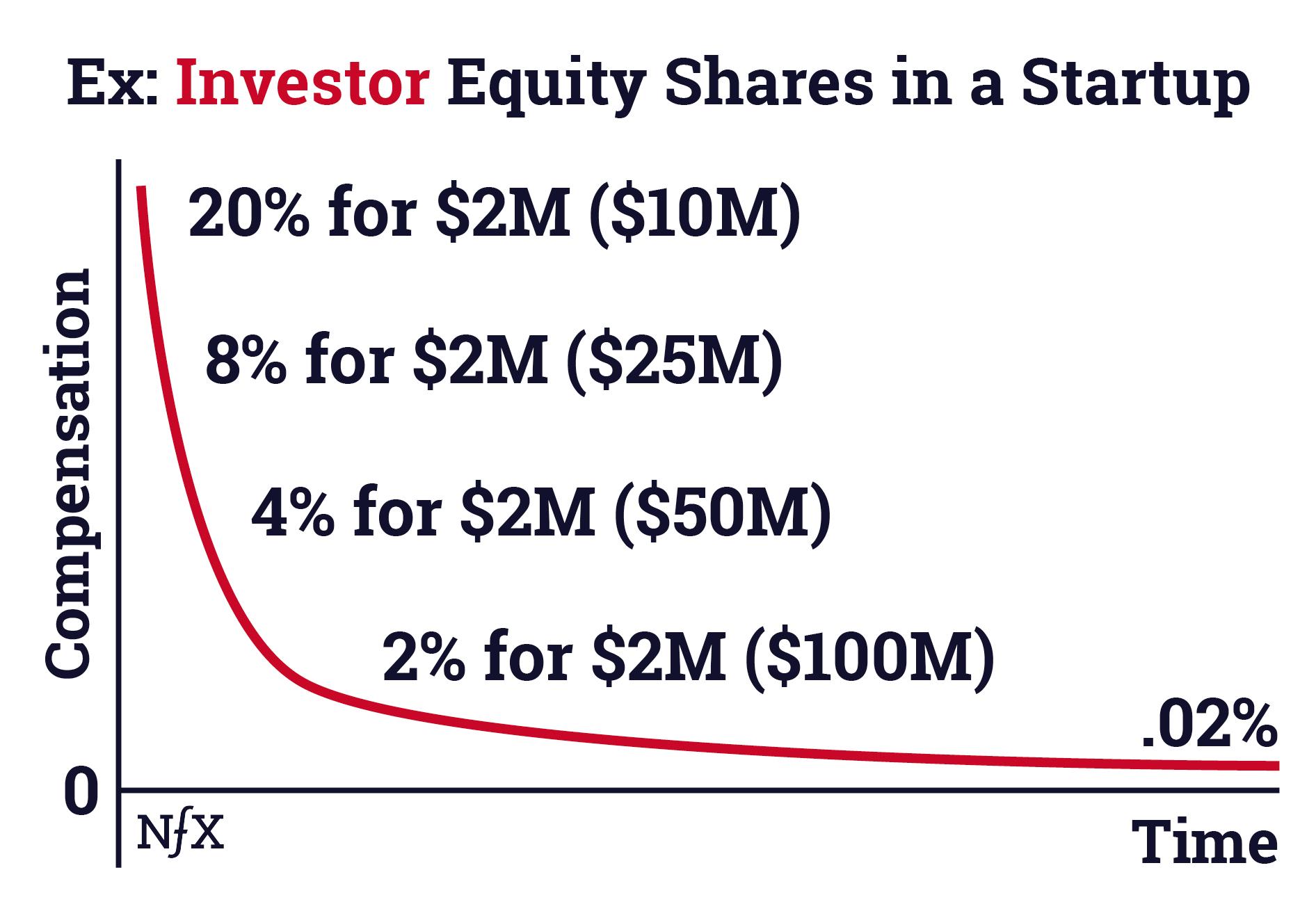

And the same thing is true for investors bonding to your startup network. Your startup pays them more equity in the early times, and less in the later times, if all goes well.

How Much Should My Startup “Pay” Each Node to Bond?

Each startup will be unique, and each will have a different network bonding curve for each type of node. That’s not as complicated as it sounds. There are some simple principles that have already become clear and only a few choices.

How much a node is worth to your network is mostly made of four elements:

- Time since inception of the network. All things equal, nodes that bond later get less compensation, and at some point might have to pay to join.

- Promise of a node’s existing network. All things equal, nodes that have the proven potential to bring more nodes, more attention, more status, more traffic, more capital, more skills will get more compensation. There is an expected benefit that powerful nodes will demand to bond initially and “vote” in favor of your project, lending their credibility and status. In the future, you could imagine formulas for this based on machine measurable stats like Twitter followers, quality/size of LinkedIn or Signal network on Signal.nfx.com, the frequency and recency of their email correspondence with other valued nodes, teams they coded on, size of fund, reach of their newsletter, reach of their audience on Twitch, etc.

- Engagement and performance after initial bonding. A node simply bonding to your network might be all you need, but in most cases, you want your nodes active on your network. If a Kardashian creates a profile on Twitter, that’s worth something to Twitter. And if she posts crazy stuff 5 times per day, that’s worth a lot more. But if she never posts, that teaches the other nodes that Twitter isn’t cool. It indicated she has un-bonded, and it will have a negative impact on the network value. So you have to design carefully for continuous bonding and engagement.

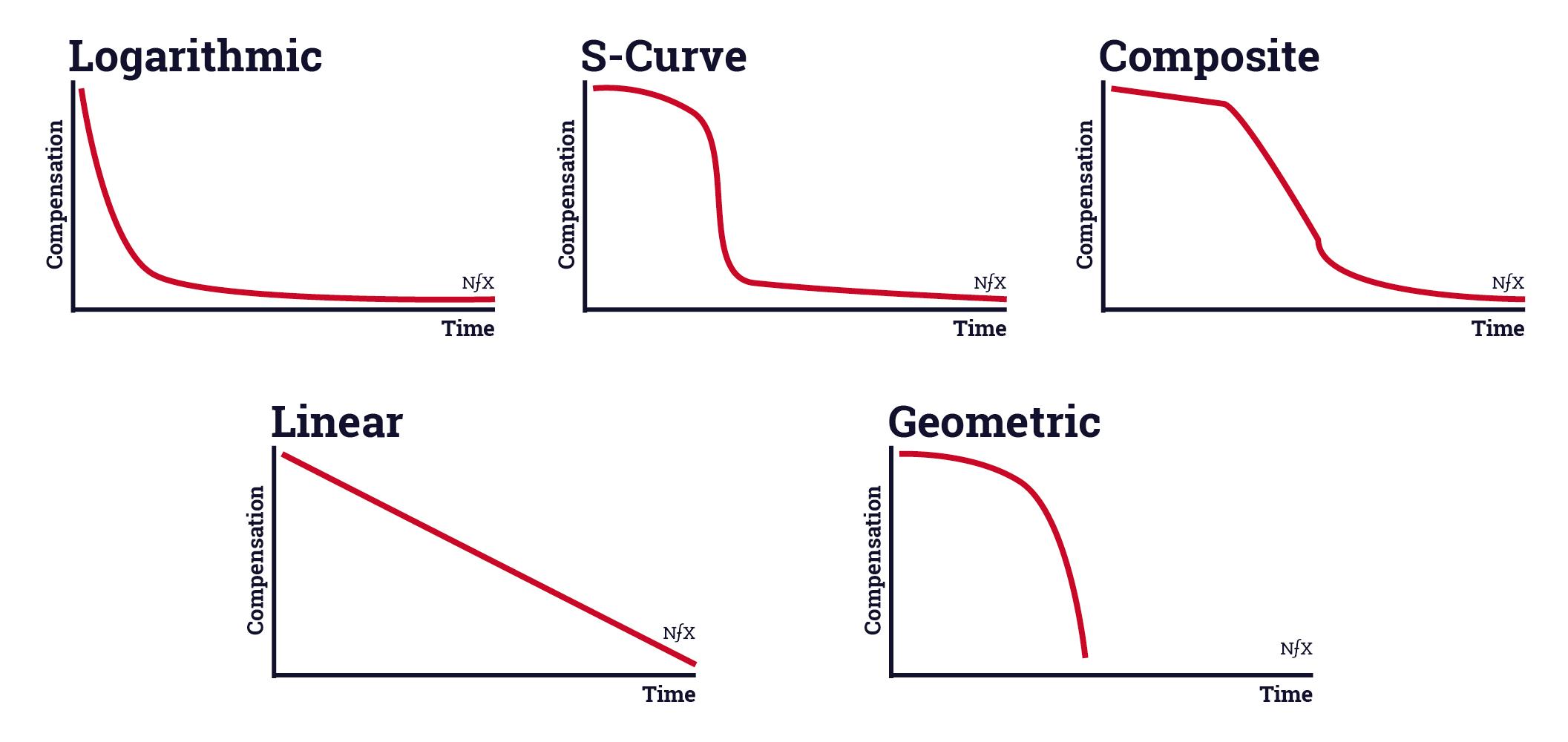

- What curve you chose. For each node type, you can choose what sort of curve you prefer. Each represents a philosophy and should be fit to the situation. You will have different inputs at different phases of the company. The formulas you use will change. You’ll need to experiment. Test the edge cases, bring them back into your formulas. These don’t need to be static. Your upfront assumptions are unlikely to be correct. We’ll all get better at the techniques and nuances of these over the next 10 years.

That being said, it seems that the top three curves in the diagram below make the most sense as places to start. The “S-Curve” in particular, lets you aggregate higher quality nodes, and not just nodes characterized by their willingness to take risk, before decreasing the compensation to future nodes. And the “Composite” has the benefit of communicating the iterative approach that might work best as situations change.

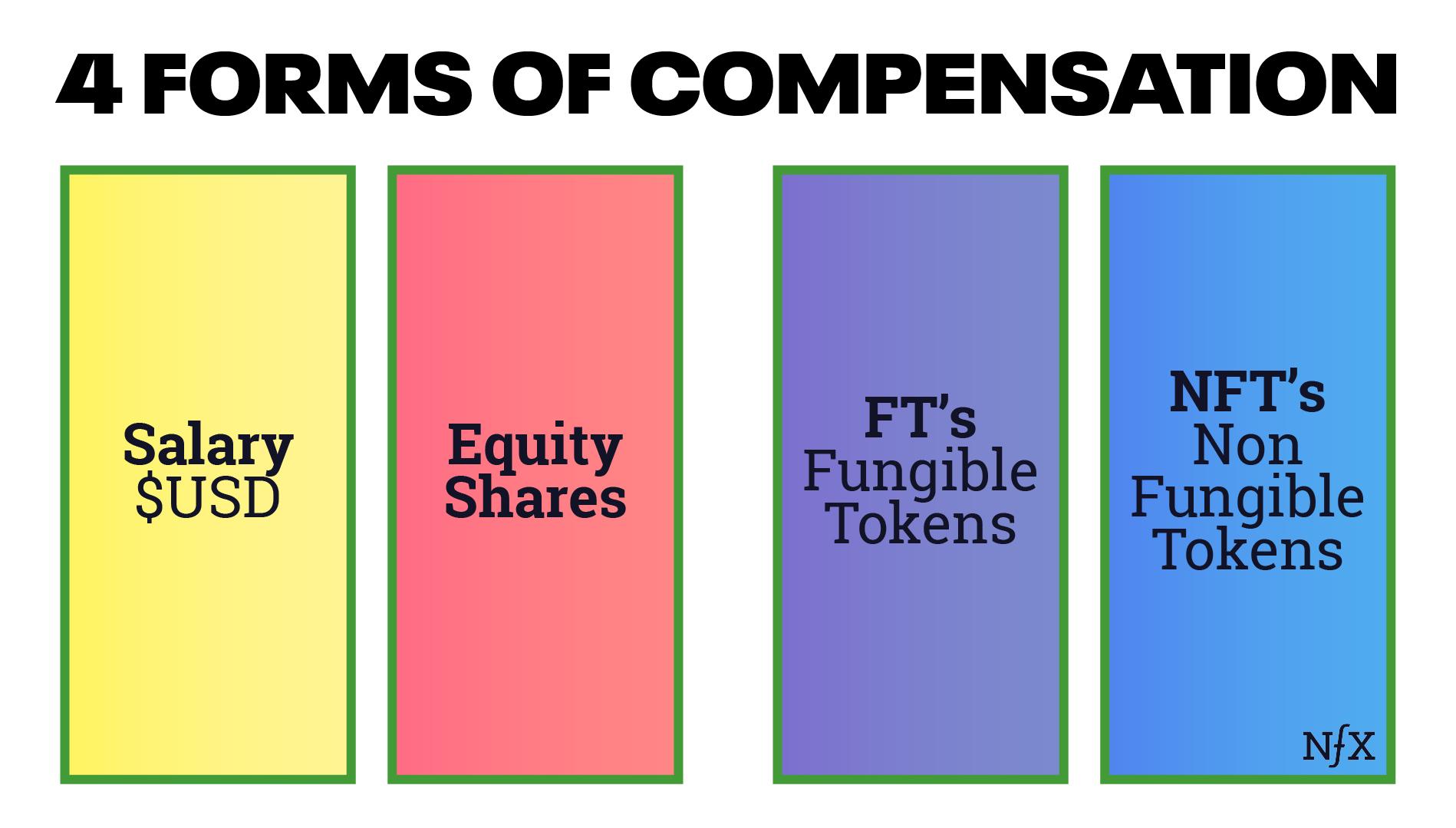

Types of Compensation for Bonding

Luckily, the types of compensation are limited. Here’s a good starting list:

- Value of using the product (e.g. utility, status, cheaper prices, fun, etc)

- Cash (e.g. USD, EUR)

- Equity shares (traditional)

- Discounted fees

- Premier placement and traffic/attention

- Status symbols

- Early access

- Some voting and/or decision making, ability to edit/change

- Premier software features

- Membership to a valuable clique of other nodes

- Real world perks like dinner/tickets to the ball game

- Belief in the mission (right-brain, intrinsic)

- Commitment to a set of human relationships (right-brain, intrinsic)

- Tokens (fungible)

- Non-Fungible Tokens

The last two should be noted. These are new to the world in the last few years, but they could play a big role in the next 10 years which we discuss below.

Again, the whole business of calculating what to pay nodes for bonding is not infinitely complex. It just takes this essay, some thinking and a spreadsheet, and you’re well ahead of anyone else in making explicit what has been implicit.

Making these network bonding relationships explicit will speed up your ability to grow your network, whether it’s the network of your company or the network of your product.

In the future, I suspect someone will build us SaaS software to manage all our bonding curves and norms will develop. Bancor already did it for certain crypto token projects and has a $800M network value. We’ll eventually have a sophisticated network valuing algorithms to determine what a node is worth at any given second.

Fungible Tokens Make Network Bonding Visible

We believe that all companies with network effects will have tokens in the next five years to help them bond nodes to their networks, both their product network and their company network.

Crazy? Not at all. This example might illustrate.

In Jan 2020, nearly two years ago, Paris Saint-Germain, a dominant French professional soccer club, worked with Socios.com to create a Fan Token, $PSG which trades on Binance, to give them a creative canvas for a modern version of a fan club, particularly for geographically remote fans.

Fans that own one or more tokens get coveted rights to things like events, special merchandise, binding votes about issues with the club, or voting on the inspiring message to be written in the arm band of the captain for the next game.

In the summer of 2021, when PSG signed a contract with one of the greatest footballers in the world, Lionel Messi, to join their team, part of the compensation was in these fan tokens. The exact amount was not disclosed but was described as “significant.” When the contract with Messi was announced, the price of the token on the market doubled. There are now 3.1M PSG Fan Tokens in circulation, out of a max supply of 20 million. The market cap is around $60m. It’s not huge but it’s a start for the industry. 43 other professional teams have launched similar fan tokens.

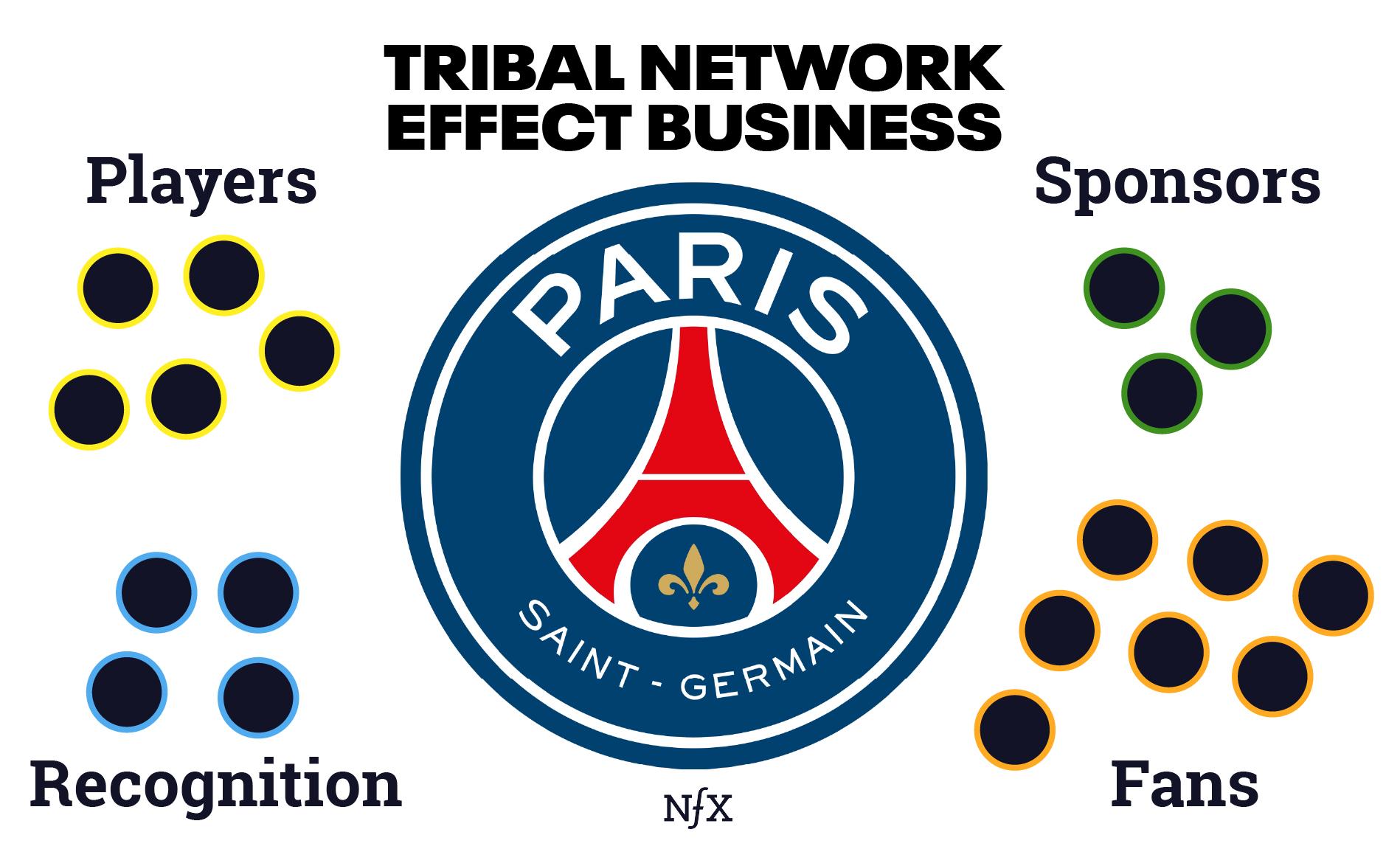

A football team is a network effect business, a tribal network effect to be precise. More fans = more fun and valuable to be a fan. That energy draws great players, managers and coaches, making the network more valuable still.

Seeing this through the lens of network bonding leads us to an interesting realization. If a professional sports team like PSG can create fungible, tradeable fan tokens and pay valuable player-nodes to bond to their network, why couldn’t they start paying valuable fan-nodes to ensure greater engagement?

Nodes are NOT equal. Nodes exhibit power law characteristics, meaning better players like Messi make a geometrically larger impact than lesser players. Like 10X engineers, we have 10X players. The same is likely true of fan-nodes. There are 10X fans, and they should be compensated to continue or increase the positive impact they have on the overall value of the network.

And what about using PSG Tokens to bond sponsor-nodes to the network? When a sponsor-node pays for their sponsorship, what if instead of sending 100% of that revenue to the team, the sponsor spends a portion of it buying fan tokens on the open market. It would signal commitment to the tribe by that sponsor, and it would drive up prices and increase the value of the tokens PSG still owns. And then the sponsor or PSG could spend their tokens to bond more nodes to the network, to draft more celebrities and characters to the network, perhaps including sponsors.

We’re making the implicit, intangible value of networks visible and tangible. Whoa. And once we can see it and move it, it becomes valuable. Out of thin air.

Once you see this dynamic with tokens, you realize we are at the beginning of a great creative era, and there are infinite combinations we can think of, some of which might work.

And if a low-tech business like PSG can do all this with a simple token and their nodes, why can’t you? It’s still early, the playbooks aren’t proven, but c’mon, you’re in the business of being on the cutting edge. PSG is 2 years ahead of you. Let’s get goin’.

Mindset Shift – Nodes Deserve Compensation for What They Add

The “Messi-node” bonding to the broader PSG network increased the value to PSG and other networks far beyond the $41M Messi is being paid per year. Here’s how I know.

Messi’s agent’s ability to ask for compensation was traditionally limited to signing bonus, annual salary, performance incentives, and a percent of merch sales. All coming in the form of Euros. Never shares in PSG.

Tokens reveal network impacts that have alway been there. Including fan tokens in Messi’s comp package to make it incrementally more accurate as an approximation to his value creation for the PSG network. The tokens doubled in value when the signing was announced, so Messi’s comp from that token doubled. This is only 2021, so it wasn’t a huge part of his comp, but in 10 years that might change.

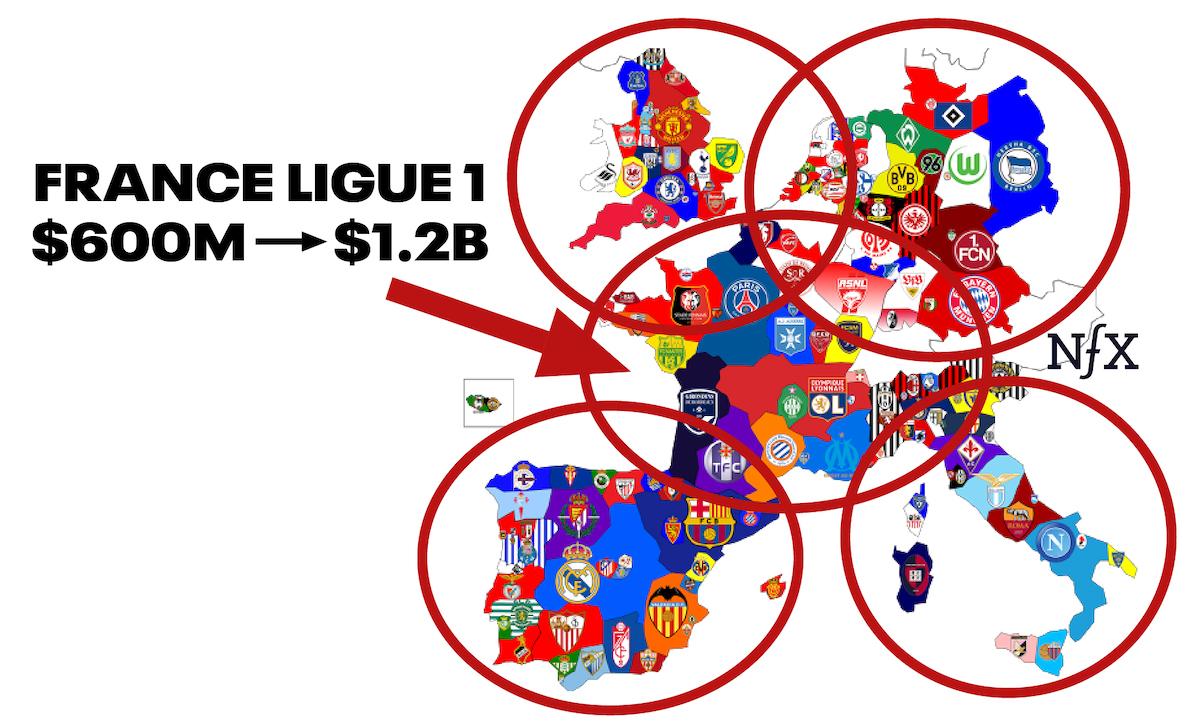

What other value did Messi create that he didn’t capture that maybe in the future he will capture? Think about the whole league network of France’s professional soccer league, Ligue 1, which has 20 teams.

As far as I know, PSG footed 100% of the bill for adding Messi to the PSG tribal network. However, by adding him to PSG, they ALSO added him to the Ligue 1 network, beating out England’s Premier League, Germany’s Bundesliga, Spain’s LaLiga, and Italy’s Serie A, all with 20 teams each.

Having Messi join Ligue 1 did two things: 1) it immediately doubled the value of the TV rights to Ligue 1 from $600M to $1.2B. 2) the other 19 Ligue 1 teams will get measurably larger exposure to potential fan-nodes around the world as they tuned in to see Messi when their team plays PSG.

To my knowledge, Messi and PSG were not compensated for this value they added to the larger network. In 10 years, I suspect these elements and more will be part of the discussion, as the people involved will have greater fluency with network theory and bonding, as well as greater ability to measure network value through software.

Now that we can start to measure the value that each node adds to a network, those nodes will begin to demand greater compensation for bonding to it.

The concept of each node getting compensated for its worth to the network will eventually be built into every piece of software that is engaged in building a network effect.

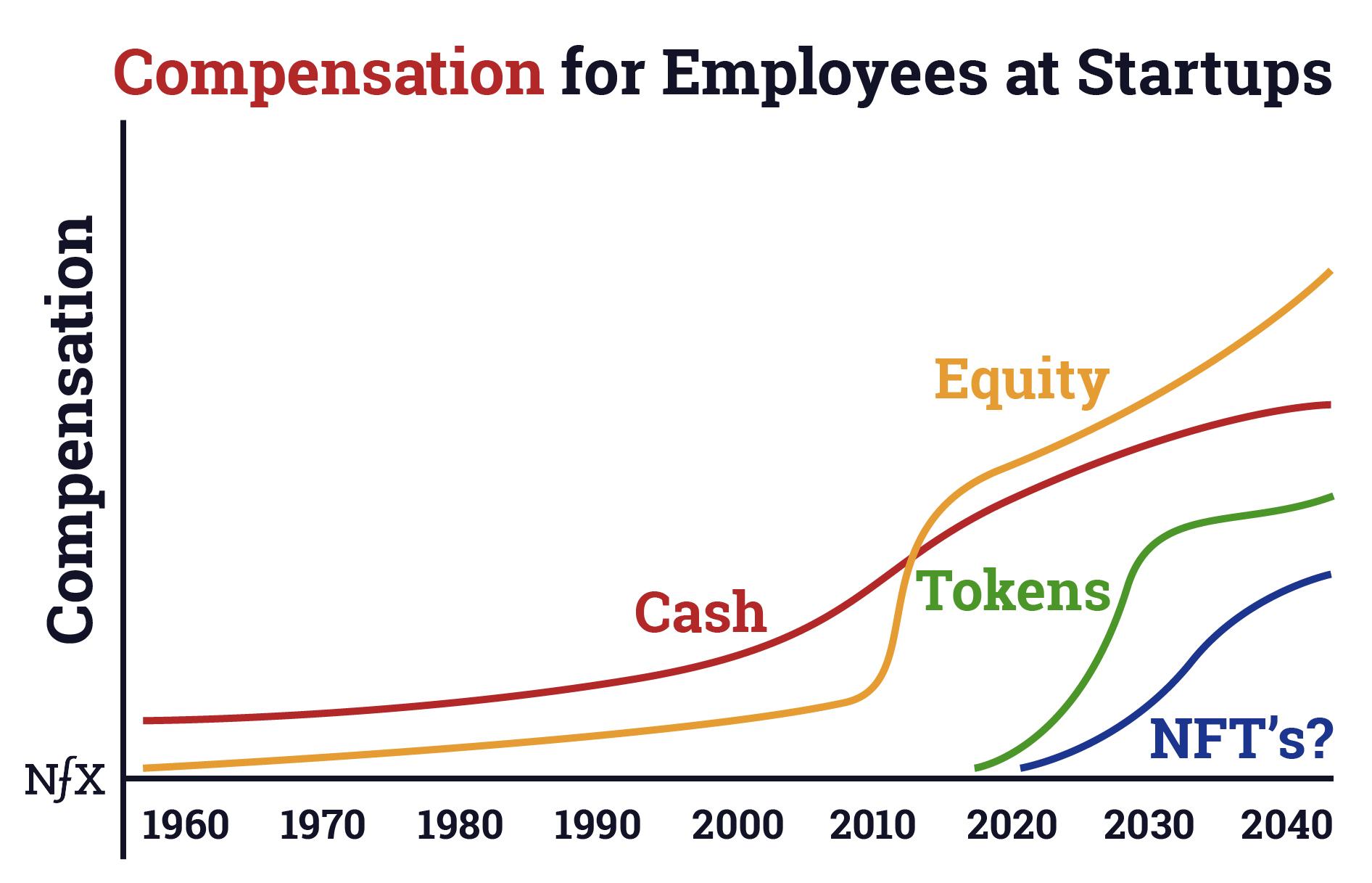

Forms of Ownership Will Change

Shares (stock options) are essentially a “token” that lets us track the growth of value of the company network.

In the past, we only had cash and stock as ways of approximating a node’s value to the network. Those were such blunt tools, so the idea of more closely approximating your network value to your actual compensation rarely came up. But now we have crypto. And that mechanism allows us to measure cheaply and discreetly, so we can now see the curves better … and that ability to see will drive this discussion.

Where are we in the arc of history on this? Shares as stock options for employees got their birth in the US with the 1950 Revenue Act, which taxed income from selling shares for a profit less than salaried income. In 1957, Fairchild Semiconductor, in the birth of the Silicon Valley mindset of non-zero-sum thinking, gave these options not just to the execs but to many of their lower level employees. By the early 60’s, when many of those employees became millionaires, the mythology was born of tech wealth through stock options. Awareness of it grew slowly, but by the 1990’s nearly every employee in Silicon Valley expected it as part of their comp package. It took until the 2010’s for that mindset to shift in places far away from Silicon Valley, like Europe. Now all tech employees worldwide understand there is a second part of their comp package beyond salary — stock and the opportunity for ownership.

The ownership economy was born… even if it has been in slow motion up until now. We predict it will accelerate from here.

With blockchain, we can already imagine two more such tokens that could grow in value alongside stock: Fungible Tokens and Non-Fungible Tokens. Not replacing, but in addition.

By adding FT’s to your company’s product and operations, as PSG did, you are creating a new token whose value will rise and fall with the fate of your company, and so these can be used to bond employees to the company network.

NFT’s might also serve that role, and we could see a lot of experimentation in the next few years. It won’t happen overnight, but it’s coming, and it’s exciting.

Warning: More Power Law Social Negativity Ahead

Initially, people will look at this move to use network bonding curves to more accurately compensate nodes for their true value as a win for the little guy. A win for the edge node that has little power today. And that’s true in part. People will get access to value through tokens and NFT’s in ways they didn’t get shares or a share of the profits before. You can think of Uber drivers, for instance.

However, I believe in the second inning, network bonding curves will also increase the income disparity at a geometric rate, similar to how we discussed all networks manifesting in “Status, Wealth, & Power: Network Effects Demand A New Social Contract.” To paraphrase:

Transparency of the value of an individual to a network creates a ruthless meritocracy. Meritocracy is good for the most talented, motivated or lucky. But for the bottom 90%, everyone can now see that they rank in the bottom 90% in performance. And the distribution of talent and success has never been equal to begin with.

Networked Bonding Curves and tokens will put the power law of unequal outcomes on steroids, as the most valuable nodes will be given tokens by many networks to bond to them. And they won’t be given a little more, they will be given a LOT more, because the math will reveal their true value to the network. Imagine how much a startup network would compensate the billionaires Oprah Winfrey or LeBron James to bond to their network.

You already see this with airdrops of new crypto network tokens to existing holders of Bitcoin or Ethereum holders, people who are most likely already wealthy. They are given free tokens with the hope they will bond to the new crypto project. This is a network bonding curve at work even though it’s still blunt today.

The visibility and measuring of network bonding curves will exacerbate the negative consequences of the power-law the Internet is revealing to us more every year. Network bonding curves are, unfortunately, another step in this trend.

Be Aware: Monetary Compensation Isn’t Enough

Network Bonding Curves are powerful new tools to create extrinsic incentives to bond people to a network. Charlie Munger says, “Show me the incentives and I’ll show you the outcome,” which sounds wise. But it’s only part of the truth.

Ultimately, networks of people are held together with heart. Not only by mathematical, transactional, left-brain incentive structures. Right brain human psychology prevails in the long term — belief in a mission, or commitment to a set of human relationships. This is why our list above of types of compensation includes 12 and 13.

We know from countless examples, that networks and companies only based on extrinsic compensation are fragile. What is strong is the combination of right and left brain psychology. The combination of intrinsic and extrinsic motivations.

If you want to read about the fragility of extrinsic-only compensation structures you can read Chapter 4 of Daniel Ariely’s Predictably Irrational book (2014), “The Cost of Social Norms: Why we are happy to do things, but not when we are paid to do them.” Also check out HBS case studies about Au Bon Pain and People’s Express.

We are likely entering a 2-4 year period where founders — Web3 founders in particular — will overshoot in their reliance on token incentives to drive their communities. Like Charlie Munger, they are right, but not fully right. We will learn a lot from their experiments and mistakes, but if you want your project to succeed, don’t forget the heart.

Conclusion

Network Bonding Theory is a new way of seeing and building network effects businesses. The tokens which have made network bonding curves more easily visible have the potential to change the nature of ownership in the Web3 era and beyond. We’ll write more about this as it evolves.

* * *

(1) The breakthrough in our thinking was triggered by our 2017 seed investment in a crypto/Web3 startup called Bancor, and also by the 2017 writings of people like Simon De La Rouviere. This small group developed a niche technique called “bonding curves” that unfortunately is now buried in the voluminous annals of the crypto blogs. (Quickly, bonding curves were invented as a way to get workable pricing for tokens in nascent crypto projects that don’t yet have enough participants to create a full marketplace clearing price.)

As Founders ourselves, we respect your time. That’s why we built BriefLink, a new software tool that minimizes the upfront time of getting the VC meeting. Simply tell us about your company in 9 easy questions, and you’ll hear from us if it’s a fit.