To help Founders with their fundraising process, we here at NFX have already built tools like Signal and Brieflink to help Founders find, connect with, and reach out to the right VCs for them.

Today, I want to share some of the non-obvious lessons I’ve learned from many years of being a 4-time founder/CEO and an investor in over 100 companies.

While NFX can’t invest in every company we meet, we hope Founders everywhere can use these lessons to put themselves in the best position possible for a successful fundraise.

A podcast version of this essay is available on SoundCloud, Apple Podcasts, Google Play, and Spotify. In addition, a complete playlist of the videos embedded below is available here.

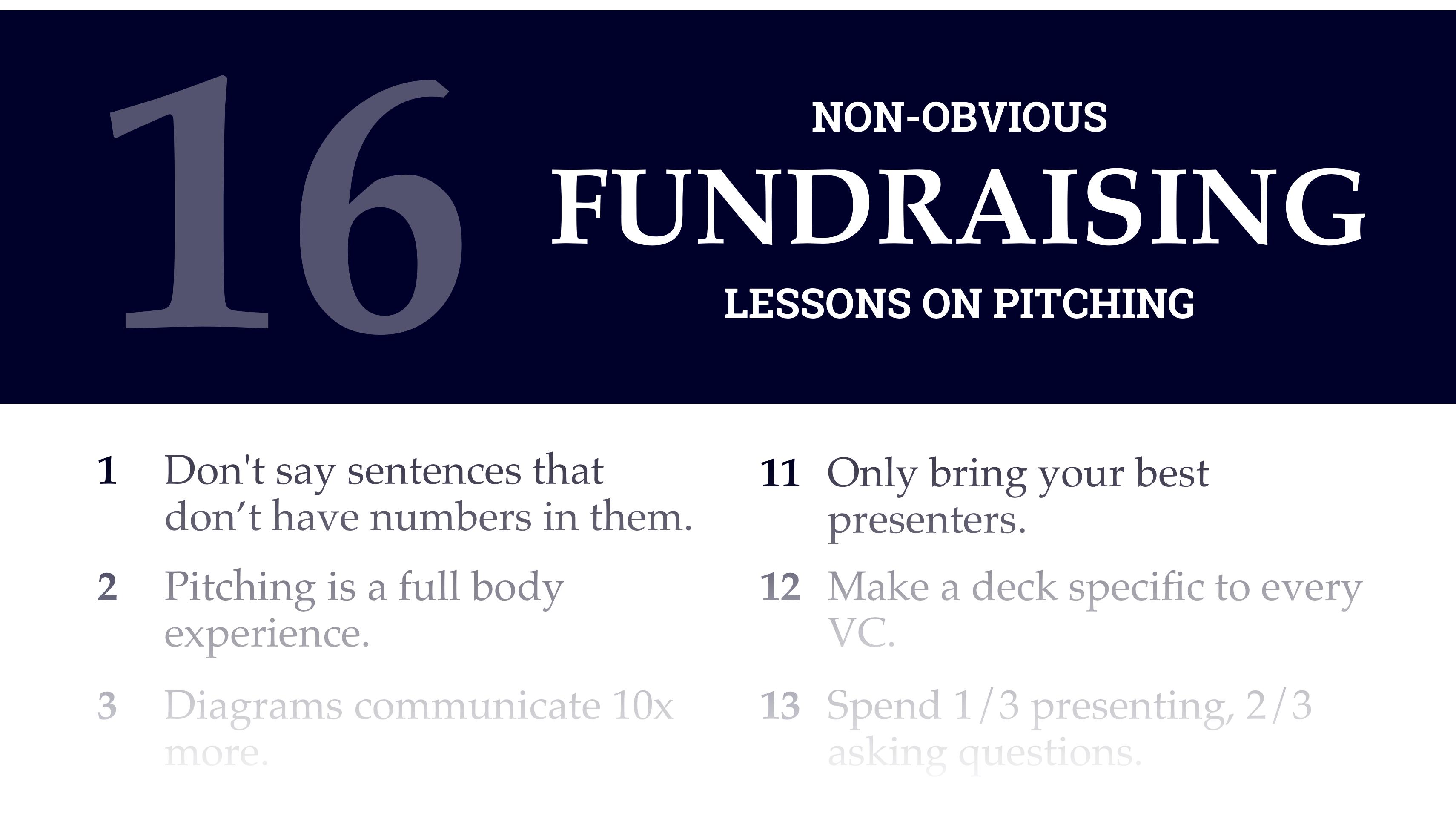

1. Don’t say sentences that don’t have numbers in them.

When you’re pitching, don’t say a sentence without a number in it. Preferably 2 numbers.

Don’t say: “We’re up a lot in the last month”

Say: “Net revenue was up 23% from between September and October”

Don’t say: “Retention has gotten so much better recently, we’re very excited”

Say: “Churn has dropped from 4.2% per month to 1.9% per month over the last six months due to 4 major improvements to the product…”

Don’t say: “There is seasonality in this business”

Say: “GMV Q4 seasonality is typically up 45% over Q3 and down 20% in Q1 again”

People who build giant businesses are data-driven people. They 1) know their numbers intimately, and 2) speak in precise numbers, not generalities.

2. Pitching is a full body experience

I see a lot of Founders that sit down for the entire duration of the pitch meeting, talking at the rest of the room like a brain on a stick.

Pitching is a performance. Its goal is to communicate tangible and intangible factors. Like any performance such as sports, or singing, or theater acting, pitching is a full-body effort. Body language is a big part of communication. Use your body to move around, or you’re not communicating fully.

Don’t make the mistake of sitting the whole time. Use your body to move around.

On any given day a VC has 6-12 meetings, which means that by the time you meet, they are likely tired of sitting there listening to people talk at them. Break the monotony. Give them a reason to pay attention. The most persuasive people use every tool available to capture a listener’s attention, including movement and body language.

Don’t be a brain on a stick. Don’t be a disembodied head. Get up on your feet and move around periodically throughout the presentation.

3. Diagrams communicate 10x more

Diagrams communicate 10 times more effectively than just words.

Sitting around hand-waving as you talk is not a good way to communicate. That’s how they did it in the 1400s. The way we do it now is with data, diagrams, and white-boarding.

Using visual tools to get your point across sharpens and speeds up the conversation. It increases the density of the information you can communicate in a limited amount of time.

You only get a half hour with VCs, and really, you only have ~10 minutes to grab them. Time is of the essence, and one diagram can do the work of many minutes of talking.

4. Jump to the screen and point

When you’re presenting your deck, get up and point to what you’re talking about.

You know your deck inside and out, so it’s easy to forget that the VC might not be following you. When you’ve got a big, complicated slide up and you’re talking about just one part of it, it’s easy for the listening VCs to get lost.

Get up out of your chair, jump to the screen, and point so that they can focus on the thing you’re focused on. Otherwise, their brain will be wandering, they’ll miss the point you’re making, and they won’t get it.

5. Send your Company Brief ahead of time

The way the introduction and meeting process currently works in the venture world is like we’re stuck in 1963. You get your introducer to send the VC an email with 2 or 3 pieces of information about you, they take the meeting, and they come into the meeting knowing almost nothing about you.

There’s a better way the best CEO’s go about it. Create a Brief on brieflink.com which includes your deck and the metadata about you that the VC needs to know to understand your business before you get in the room.

That way when you get to the meeting, you can actually get to the heart of their concerns and interests in your business. Otherwise you’re going to spend the first 20 minutes going over the basics: e.g. where’s your HQ, how many employees do you have, what’s your traction, how do you make money, etc.

If you use Brieflink, you can get VCs all that information ahead of time. You can basically have the second meeting with them on your first meeting, which will save you time and make it more likely you’ll get funded — and much more likely you’ll get something valuable out of the meeting regardless.

Further, if they have all your information, they’ll be more invested even before you walk in the room. If you’re just using a deck or an email, you’re way behind the entrepreneurs who are using Brieflink.

6. Get there 15 minutes early

Arriving fifteen minutes early lets you set up for your presentation, get your deck up on the screen and working, make sure the whiteboard pens have ink in them, check all your dongles, and in general getting prepared so that your presentation goes as smoothly as possible.

Too often I’ve seen meetings derailed by logistical mishaps or being late.

So do yourself a favor and invest an extra fifteen minutes into your pitch meetings by getting there early. That way you protect not only the time you spend in the meeting, but the travel time to and from the VC, not to mention all the prep time you put in. And more importantly, you won’t end up checking off one VC from your shortlist of potential investors for no good reason.

As one mentor told me, “Everything good in my career has come from arriving 15 minutes early.” Fundraising pitches certainly qualify for that treatment.

7. Sit in the front of the room

VCs are creatures of habit. They get 6 pitches a day 200 days a year, and they come and sit in the same chair, in the same room, over and over again.

Figure out where the VCs are positioning themselves in the room, and make sure you’re in front of the screen that you’re using to present your deck.

That positioning is critical so that you can get up, interact with your deck, and be dynamic, engaging the listener during your pitch.

Engage with your material. Show your excitement. And put yourself at the right spot in the room so that you can make that happen to the best of your ability.

8. Don’t talk about your passion – show it

Years ago, I was in a pitch meeting when I worked at another venture firm. The Founder was losing the investors and the pitch was going to fail.

Realizing this, he got down on one knee, looked the top Partner straight in the eye, and said, “We are going to make this happen, because this is my life and I know the market better than anybody.“

That passion and energy woke the partner up and got his attention. Eventually, we invested in the company. I don’t know if it was just the knee bend that did it, but the way he showed his passion, instead of just saying “I’m passionate” definitely factored in.

Project your passion during your pitch. That doesn’t always mean getting down on one knee, but words alone aren’t always enough.

Show that you’re a full-blooded person that’s going to drive the business forward through strength of will.

9. Look the part

Wear something nice, sharp, crisp, and shows you’re serious about being a professional.

I’ve seen people come in with sweatshirts and frumpy pants, and they sit down with their coffee and their snack and their laptop, and it’s just a mess down at their end of the table. It doesn’t look professional.

If you present like that, it’s hard to believe as an investor that you’re going to run a competitive business and eat everyone else’s lunch.

Make no mistake: you’re in a highly competitive industry. 25 years ago, there were a few VCs and a few thousand startups. Now, there are millions of startups. Wear something sharp to help signal you’re a top competitor.

10. Bring a pen and take notes

When you come to a pitch meeting, bring your laptop and a notebook and something to write with.

When the VC says something that you want to remember or get back to, you can use the pen to not only write it down but also to show the VC that you’re taking notes.

Why is this important? 9 out of 10 VCs typically won’t invest in you. That means that 9 of them are going to end up being free consultants to you. If you don’t take the opportunity to learn from them and ask them questions, then you’re doing yourself a disservice.

Not only that, but if you’re not taking notes during these meetings, ultimately your overall fundraising process won’t work.

Here’s the thing: you can’t look at each individual meeting as do or die and think “I have to get this investor’s money”. Instead, you have to think: “I have to have a successful fundraising over the course of 10 or 20 potential investors.

In light of that, every meeting becomes an opportunity for you to improve your pitch, learn more about your business, and learn more about your competitors. That’s what will lead to a successful fundraising.

And to do it, you have to ask questions and take notes. Having a pen and paper there can be a good visual reminder that during the meeting you need to pitch in 10 minutes and ask questions for the rest.

11. Only bring your best presenters

Who to bring to the meeting can often be an emotional thing among you and your co-founders and teammates. Many people would love to be in the room to help. Thus, this can require you to have some hard conversations.

Everybody that you bring to that room needs to be as compelling as you are, everyone needs to have a role to play in the pitch, or they should not be in the room.

There are some people who are very good at pitching. They’re good at getting the energy level up, speaking concisely, and answering the question that’s being asked. And there are some people that aren’t.

You can’t bring the people who aren’t good at pitching to the meeting. Your co-founder might be great at whatever their role is, but it’s unlikely they’re equally good at pitching. If you’re good at pitching, don’t bring them in because it won’t set you up for success.

If you have team members that will add to the pitch, then, by all means, bring them. But it’s based on their personality and their skill in pitching. It doesn’t necessarily reflect their role or status in the company.

12. Make a deck specific to every VC

Using the same deck for every investor is a mistake I often see Founders make.

When I was fundraising, I had a different deck for every pitch I made to each individual investor. At the end of my fundraising process, I would have 60 decks for 30 different investors I was pitching.

It’s important to tweak the language in your pitch for each VC depending on what they value. When you come to us, for example, if you include slides and analysis around the network effects in your business, it’s easier for us to get interested.

Similarly, for other VCs that are big on other things, your deck should capture the opportunity to show them how what you’re doing fits in with the things they already know well and can have good judgment on.

This is especially important because when you’re pitching a VC, you have to arm them with the language to convince the other partners in the firm. The partner you connect with may get as little as 30 seconds at the weekly partner meeting to explain to the other partners why they should even discuss your company rather than other companies or pressing topics.

Use language that will arm the partner you’re pitching to persuade everyone else at their firm.

13. Spend 1/3 presenting, 2/3 asking questions

If you have a half-hour meeting, that means you have about 8 minutes to get through your deck. Don’t think of the whole time of the meeting as the whole time that you’re pitching. You’re pitching for 8-10 minutes and the rest of the time asking questions and discussing with the investor.

VCs often have meetings back to back all day long. Understanding and working with those time constraints is key. Expect a “half-hour” meeting to really be 25 minutes because of delays and other things beyond your control.

Investors want to understand what’s great about your business. They’re hoping that you’re the one they can invest in this year, or this quarter, whatever their cadence is. Give them the time to find out by planning ahead, being prepared with questions, and not spending the whole time going through your deck.

14. The goal is learning, not closing

It’s worth repeating: you’ve got to ask VCs for feedback during the meeting. It’s probably the most important part because you have to assume they’re not going to invest in you.

Be clear on the mathematical reality. Seed VCs look at 1,000 companies per year, and they might invest in 4 or 5. For Series A investors, it might be as little as one or two investments per partner, per year.

Given the math, it only makes sense to assume you’re not getting investment from the VC in your pitch. But what you do have in the room with you is someone who has seen hundreds of business plans, hundreds of patterns of failure or success over the years, and they’re available to you right now for free.

Think of them as someone who is not going to invest, but who you’re going to get valuable information from by getting them excited about your business and asking them the right questions.

There are so many interesting questions you can ask a VC when you’re there in the room with them, and most of them can give you insights that you might not have thought about before.

Having good questions about the firm shows you’re doing your homework and that you’re selecting your VC carefully. This kind of diligence shows you’re the type of quality thinker that’s capable of building a giant company.

15. Know when you’re improving or not

Your pitch can evolve significantly over time as you learn more about how it’s being understood by investors. You might not change your business much due to investor feedback, but while pitching, you should learn a lot about how to communicate your business. Your pitch should continually improve.

If you can feel that VCs are getting more interested as your pitch improves, stay on course. If, however, the feedback you’re getting is that there’s low interest, and it isn’t improving, then it may be time to start making more significant adjustments to team, market, product, and go to market. You want to stick with your unique vision, but also take the opportunity to learn.

The other option is to build your business without VC money and prove it out by bootstrapping. VC money is just one of many ways to finance your business.

If you plateau in your fundraising, you have to be courageous enough to think from first principles: am I in the right spot? Am I in the fast-moving water? Is this the right time? If the answer is no, then perhaps go back to the beginning.

16. Understand VC Psychology

If you put yourself in the VCs shoes and understand the constraints and the context they’re operating in, it’s a lot easier to take things less personally. It also lets you pitch more effectively if you can understand your audience.

There are three major things to know about being a VC the molds their psychology coming into these pitch meetings:

#1 – VCs are being pulled apart in 360 degrees

Being a VC can be repetitive, like being on a manufacturing line where the companies come by one after the other, and the VC has to decide on the quality of each part day after day.

Deal quantity is a big part of being a VC. They process a large number of companies that come inbound from many relationships that require attention: other Partners at their firm, portfolio CEOs, friends and acquaintances, former co-workers, other VC friends that want them to fund the next round, etc.

VCs are constantly switching contexts. In addition to looking at new deals, VCs have to allocate time to work with portfolio companies, help them with their fundraising, help them recruit, help them get press. They need to meet with their own investors or potential investors in their next fund, to managing HR in their own firms, the operations, the marketing. They need to weigh in on legal documents on their investments, often many are going on at once. The banks need something approved today, a journalist needs a quote today. The number of directions a VC is being pulled in is significant, like running a startup itself is.

#2 – VCs have to say no all the time, and it wears them down

Because a VC has to say no for 99%+ of the deals they see, their minds are being trained to be negative. They are thinking about what could be great about a company, but also they have to think about what are the signs or red flags that this company wouldn’t be as big as they would hope it would be. They often come off as rude or cold because of this.

In order for them to get to the no 99%+ of the time, they have to hone and develop their negative mental muscles, to quickly see what’s wrong with an idea or a team.

Over the years, if the VC doesn’t guard against it, this wears down on them and makes them cynical, distant, and cold. Like with doctors, if they emotionally connected with everyone they meet with every day, it would be too exhausting. So they keep their distance.

But keep in mind that they want to say yes. They want to believe in your company and invest, and they want to support Founders. That’s the exciting and fun part of their job. Unfortunately for them, the majority of their job is saying no to Founders.

#3 – Being treated like an authority figure instead of an equal

When you go into these meetings, don’t treat the VC like an authority figure.

Just because you’re asking them for money doesn’t mean they’re above you. They’re peers of yours. They’re just entrepreneurs trying to build their portfolio — that’s their entrepreneurial activity.

You are entrepreneurs talking to each other to see if there’s a potential biz dev deal between the two of you. You need to treat them like equals and have the confidence to have a real conversation and be authentic with them.

Stop looking up to them because they have something that you want. The more you can show maturity and confidence, the better the pitch will go.

As Founders ourselves, we respect your time. That’s why we built BriefLink, a new software tool that minimizes the upfront time of getting the VC meeting. Simply tell us about your company in 9 easy questions, and you’ll hear from us if it’s a fit.