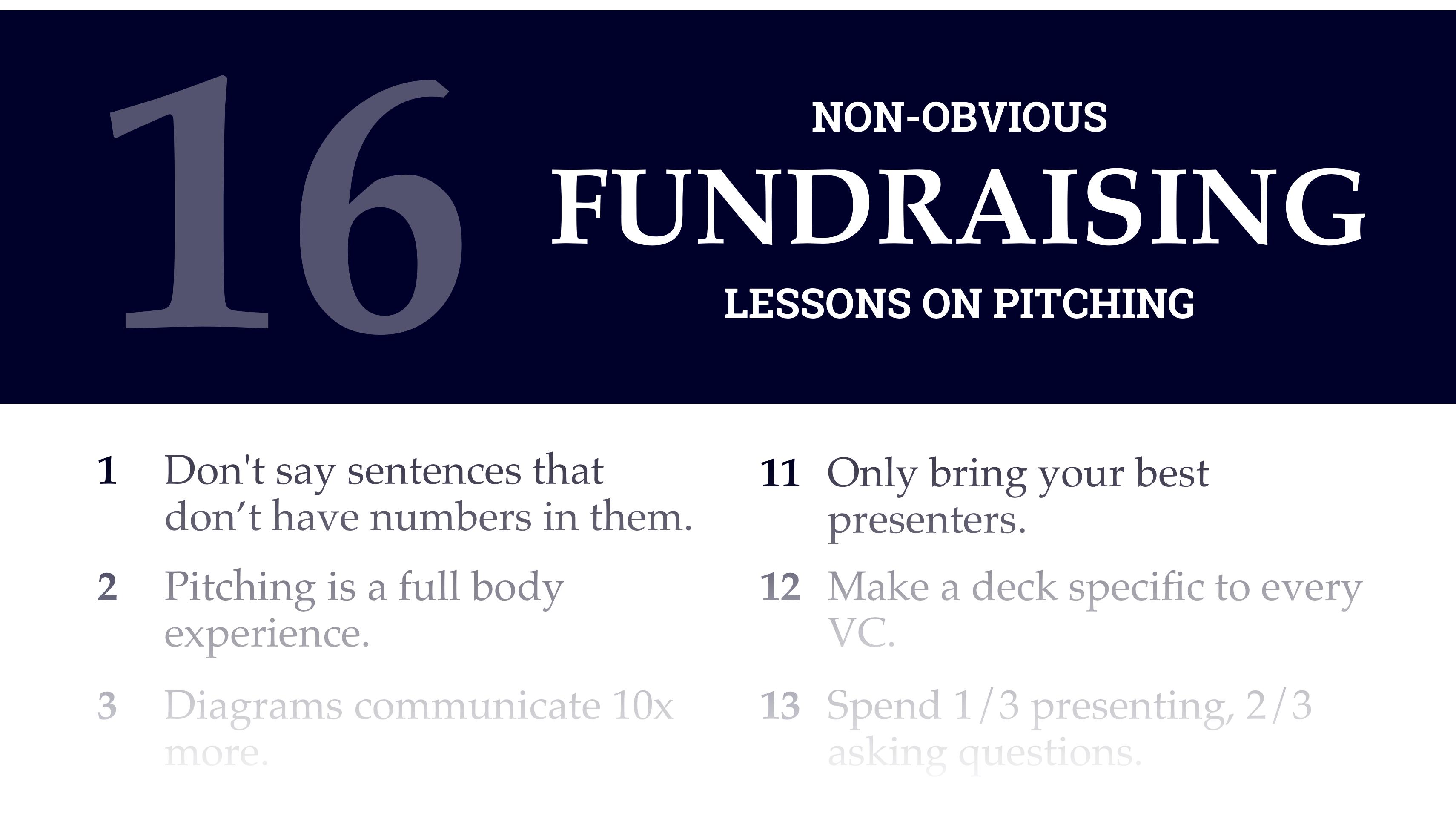

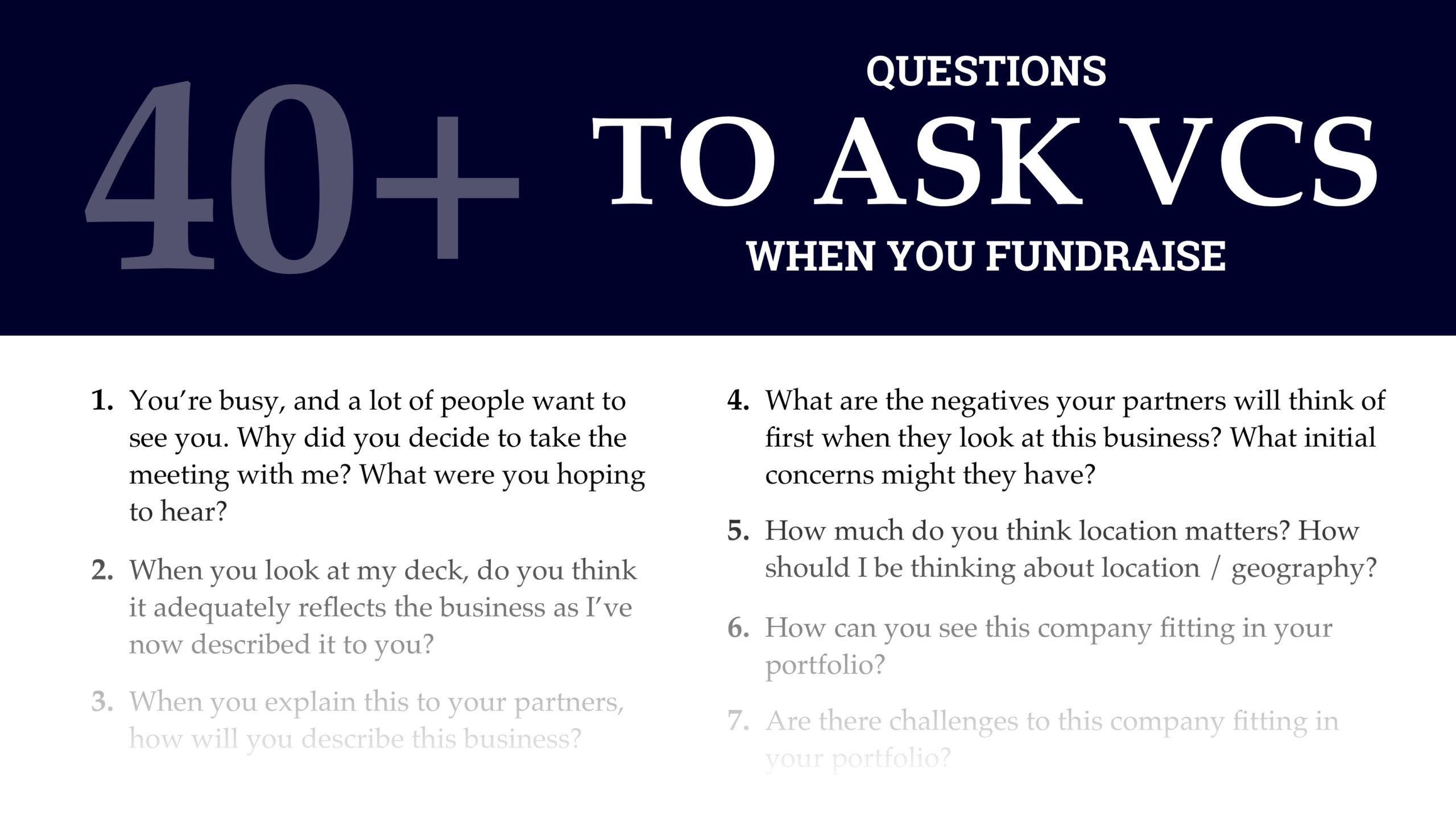

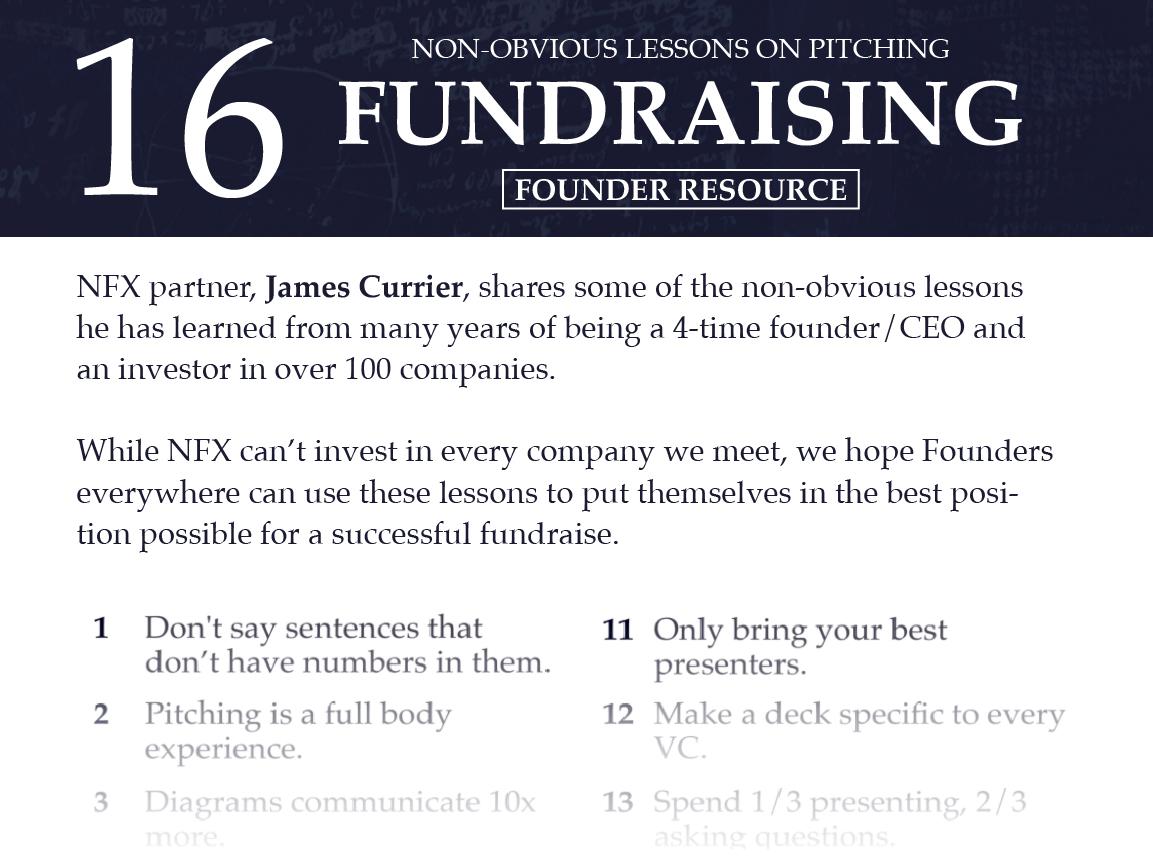

In our essay on how VCs decide to take a first meeting, we wrote that “a typical VC might get introduced to 1,000 companies per year, meet with 200, and invest in 4.”

But 2020 is not a typical year. It has ushered in a new remote era for the startup ecosystem, changing the nature of fundraising meetings and decision-making. VCs are now evaluating companies without ever meeting in person, and Founders are adapting how they get connected to investors — and pitch them — as a result.

To help Founders better understand this new world, we asked top VCs what successful tactics they’ve seen Founders use, as well as how they’ve altered their own investment processes.

At NFX we have long believed that Founders deserve a better fundraising experience — one that is tech-enabled. That moment has arrived.

Now, the Founders who excel in networking, pitching, & fundraising online will have the strong advantage.

Gigi Levy Weiss, General Partner @ NFX

Request short meetings, and invest in high-quality video + audio

The way to get meetings hasn’t changed — the best still manage to get warm intros. It does seem, though, that with more time at home and more research time, the quality of the cold emails I am getting has improved. They are more researched and personalized, which is good.

A new tactic I’ve seen is to request very short meetings. I now often get requests like ‘give me 15 min to demo the product and I am sure you would love it’. Before, that would have sounded like a strange request in a physical meeting world (why would the Founder settle for 15 min if they are making their way to find me?). But it’s a valid suggestion today. And, as it’s a smaller request, I say yes to more such requests than I did before.

Pitches essentially remain the same, but this new presentation arena has forced them to be more effective and more concise. The video medium gives more control to Founders and allows them to better control their pitch — which I think is a plus.

On the flip side, they can’t demonstrate their energy, jump to the whiteboard, or read my body language — all these are bad both for me as an investor and for them as they “normalize” everyone to a similar energy level and body language.

Top Founders are coming ready with many more backup slides (as it’s tough to draw on the whiteboard), are demonstrating their energy on the pace of speech, and are moving between different presentation modes.

Many Founders are also becoming more aware of the importance of their video and audio quality and are investing in tools to make sure it’s high quality. This makes a big difference.

Running through a full deck is not easy on video, so more smart founders are sending the deck ahead of time and asking what I would like to discuss in the call. That’s very helpful too.

Last thing: in many first meetings it used to be just the CEO. Now with the low burden of the video (not having to travel to the investor’s office), many teams are showing up 2 or 3 Founders to the call and are much better coordinated on who is presenting what. When executed well, it’s a great improvement to a solo meeting.

5 tells I look for in video calls

As I am not able to read as many tells from the people I meet remotely vs. in person (such as how they walk in, how they say hello to the other people in the office, do they take their glass at the end of the meeting, etc.), I use a few methods to try and fill in the gaps:

- I check how well they prepared for the video meeting and look at the quality of preparation as a tell sign — including video and audio quality, backup slides, etc.

- While the Founder will be trying to control the flow, I will be asking questions and taking the discussion in the directions I care about more, not just to get the replies I need but also to see how the Founder is dealing with the changes.

- When a team is showing up, I will pay a lot of attention to the team dynamic when hard questions are asked. The way the team handles the stress is very important and is very visible over video.

- I would take the time to do further video meetings with other team members who I might not have met in person. Even if it’s for 5 minutes each. In a way, I’m going wider (meeting more people) where it’s tougher to go deeper (having intimate discussions face-to-face).

- Last but not least — I continue having small talk before the meeting (the first few minutes) as if it’s a face-to-face meeting. Many founders are surprised that I don’t just jump into the discussion — but the small talk tells me as much as the actual discussion does.

The 3 Types of Pitch Emails

Gigi’s lessons from Brieflink, the tool to pitch your company to top VCs

- There are 3 types of pitch emails I get: Generic, Superficially Personalized, and Truly Personalized

a. Generic emails: It’s very clear when the Founder sent the same email to 50 or even 500 different investors. When I get something like this, I’m unlikely to be interested. It shows a lack of understanding of the fundraising process, which hints at broader ineptitude with sales.

b. Superficially Personalized emails: The first sentence or so may be personalized to me. This gets me across the line to at least read the email.

c. Truly Personalized emails: These are the types of emails that get the most attention from investors. It shows the Founder has put the work in to find out what I’m investing in, what I value, and embed this into the email they’re sending me. - An email that worked for getting the meeting: A Founder once wrote me a full analysis of my investments which were adjacent to their startup, and explained why it made sense for me to invest in them as a result. This really made me want to meet them, even though I ultimately didn’t invest.

Mark Suster, Managing Partner @ Upfront Ventures

Focus on getting access, getting a “yes” & making an impact

It’s clear that social norms have changed as a result of Covid-19. Given how few investors are actually meeting people in public, it can be daunting to figure out how to get access and how to build a relationship over time with a VC when you know you’re not going to just bump into them at an industry event or conference.

The first thing I’d like to point out is that many investors ironically have more time available for meeting Founders because they aren’t spending time commuting, flying on airplanes, or attending conferences. At the same time, while VCs have more capacity to meet, they are also pretty ‘Zoomed out’, so it may be harder to get a VC to want to commit to yet another video call. So here’s my quick advice on how to get access, how to get a ‘yes’ for a meeting, and how to make an impact.

Getting access: Investors are inundated with meeting requests and have to make decisions about whom to meet and who unfortunately will not get a meeting. If an investor has to spend too much time thinking about whether to meet you or not, the chances of getting a meeting are greatly reduced. That’s why introductions are so critical. If a founder whom I already respect suggests I meet with you, the chances of my saying ‘yes’ are much higher because I’m taking advice from somebody I already trust. It isn’t that hard to network with early-stage founders, so my advice is to spend your time getting to know founders who have raised Seed & A rounds from VCs and over time earn the right to get introductions.

Getting a yes: If a VC assumed he or she would need to allocate a full hour to meeting you, the chance she says yes is greatly reduced. So make sure that you ask for an ‘introductory meeting’ in which you promise for the first call to be short, sharp and to the point. Offer a 30-minute meeting but don’t schedule anything for 45 minutes behind that in case he/she wants to run over. Have a game plan for how you want to use all 30 minutes in a high-energy, thought-provoking discussion.

Making an impact: I already gave it away — make an impact! Make it very clear early in the discussion what you do and why it matters. Practice your pitch so that it’s high energy and has a narrative. Have your points be staccato so that an investor can jump in to ask questions, or make a point themselves. In the meeting, inform the investor of your planned time frame for fundraising and your planned process. Close the meeting by asking whether your company fits the criteria of what the investor is looking for and how this pitch resonated or not with the VC.

What you’re doing is forcing the investor to think about how they viewed you and by verbalizing it out loud they also begin to think about that themselves. If it’s not a good fit, better that you know now. If they think it’s a good fit, then ask for a next step. My preferred ask would be, ‘Do you mind if I email you a short update with how we’re doing in 4-6 weeks from now?’ This is your hook to stay in touch and to earn the right for a second meeting.

Remote relationships are easier to build than I expected

As an investor, you would imagine it would be harder to make investment decisions without meeting teams in person. In some sense, this is true because we don’t have the ability to “kick the tires” of the office and staff and get a sense of the team and culture. But for Seed and A-round investors like Upfront Ventures, in many ways, I find the current environment easier to evaluate investments.

As a starting point, it is much easier for both parties to agree to have 5+ meetings in rapid succession to iterate around various topics of discussion because each meeting doesn’t require a commute or a commitment to a full hour. These fairly intimate conversations (on a Zoom, looking into each other’s house) actually help with rapport building, which is critical to evaluating — in both directions — whether or not we want to work together.

The hardest thing for me to evaluate is the interplay between founders. In a group setting, I often ask questions and then watch how the founders interact with each other. So much about the success of an early-stage business is the founder-to-founder dynamics, so this is critical. But having less insight here is accommodated for when I’m able to get to spend more time getting to know each founder individually.

In general, I find the remote relationship building much easier than I had expected.

How to find the right VCs for your startup (Mark’s lessons from The Brief)

- One of the most valuable things that Founders have is your time. Yet when people go out and fundraise, they often just take random introductions and start taking meetings. I don’t recommend this.

- There’s an old saying: “measure twice, cut once.” The amount of time you put into pre-planning your own fundraising process really matters.

- As an example, here’s how we fundraise ourselves, as investors:

-

- First I look at LPs and try to qualify the ones that have invested in funds our size. I start with a list of 800 names — you can get databases of who VCs are — and create a reduced list of investors who’ve invested in funds similar to mine.

- Then I look for places where I know somebody who has raised money from them directly, call them up and ask them if they think they’d be a good fit for me.

- I create a qualified list based on that feedback and only then ask for introductions.

- Finally, I look for subtle cues along the way to qualify investors further based on who leans in. It might mean that 2 out of every 3 drop out, but for the one that leans in I have a much better probability.

- Important: Never take a meeting that’s not based on an introduction. If someone sends me a high-quality introduction, when I start the meeting, I’m leaning in, thinking “this is going to be great.” If I take a meeting without a quality introduction, I tend to start the meeting leaning out.

Ann Miura-Ko, Co-Founding Partner at Floodgate

How to think through Founder/VC Fit

While so many things in life have changed during shelter-in-place, I’ve found that it has given renewed focus to what matters — both personally and professionally. For founders approaching venture firms for financing, this is a great opportunity to make sure that there is a fit between the investors’ interests and risk profile with what a founder is trying to accomplish. The better a founder has thought through this fit, the more likely they are to stand out. I have moved to a model where often I will first ask a series of questions first.

- How much are you raising? As a founder, if you are raising a $10M Series A and you’re looking for a partner to lead this round, we are not going to be the right partner for you. This is an easy pass. For Floodgate, we are looking for pre-seed or seed as our core sweet spot writing checks that range from $350k to $3M.

- Where are you in the process? If you need an answer today, you are better off talking to angel investors. Since we are typically lead investors, we generally need about two weeks from first meeting to get to term sheet. Even with the efficiency of Zoom meetings, we actually will want to get to know you as founders and would expect you to want to do some diligence on us. Make sure you leave enough time to get to know the investors who will be on your cap table.

Showing that your startup is venture-backable

These next few questions are more about your core business and tells me the narrative of who you are and — very importantly — why venture capital is the right financing mechanism for your business. It also tells me a little bit about why seed stage investors will be rewarded for the risk they take in investing in your business.

- Why this? Of all of the things you could be working on, why choose to work on this? I like to understand the narrative of the founder and what has caused them to commit to this business.

- Who is on your team? What are they experts at?

- Insight. I like to spend a lot of time here learning about the founder’s insights, which generally tells us if something is venture scalable or not. It also tells me if a seed investor has any business investing in the business at that stage or not. As Jeff Bezos said in his congressional hearing statement recently, “Outsized returns come from betting against conventional wisdom, but conventional wisdom is usually right.” What is the piece of conventional wisdom you’re betting against and what do you get for the risk that you’re taking? In other words, you generally have an insight about the market, technology, or regulatory space — that most people may not know or understand — that gives you a massive advantage / acceleration into the market if you are right. What is this insight? (By the way, many founders are left scratching their head when early-stage investors say they need to see traction. This is just another way of saying you don’t have a unique insight, so there is a lot of potential competition in the landscape. The only point of differentiation ends up being traction.)

It is actually quite rare to get exceptional and thoughtful answers on these questions. I feel that this perspective is probably more timeless than just focused in a time period where we are all on Zoom. That said, the reason I bring these points up now is that I think focus is becoming more important. Rather than casting the net wide, you want to make sure that there is a great fit, right up front. We should all be going for the no as quickly as possible so that we can get to that heck yeah when it matters.

Find out if the VC has a passion for the space (Ann’s lessons from The Brief)

- One of the most important factors to whether or not I want to take a meeting with a Founder is if I have personal passion for what they’re pursuing.

- That can be hard to tell from a Founder’s perspective, of course, because there might be new areas of investment that an investor is looking at.

- The problem with me investing in a space I’m not passionate about, especially at the really early stage, is that I basically want to be co-conspirators with our Founders — and if I feel no passion or love for the idea, that’s going to become an obstacle for me becoming a true co-conspirator.

- My interest in the space is also linked to how large I think the market is.

- Also relevant is how authentic the story of the Founder is relative to the problem that they’re trying to solve. If it’s a problem that you whiteboarded while you were brainstorming startup ideas, it’s probably going to be a little less compelling than where the Founder found authentic pain through their own personal experiences.

Charles Hudson, Founder & Managing Partner @ Precursor Ventures

Founders have adjusted to the new normal of remote fundraising

We have been investing in Founders on Zoom and the phone since the beginning of Precursor, so this isn’t particularly new for us. Ironically, our standard meeting is a 30-minute Zoom meeting for first introductions, which is the same as it was prior to SIP.

I do think that pitches, where people have a good setup (good lighting, a good microphone, and audio and a strong Internet connection), goes a long way. I like a simple deck with a clear story presented by the Founders.

I think Founders have really adjusted to the new normal. In general, I think people have standardized on Zoom plus the deck, and I think that new normal makes it easy to be consistent across meetings.

The one thing that does feel different is that we have been able to compress the time spent in between meetings, in some cases, because nobody needs to travel to have follow-up meetings.

Being ‘in the room’ is not a priority

Maybe we are unique on this front, but we have never prioritized being in the room with Founders as part of our investment process. In a way, this has been a relief to be in a world where lots of other people are coming to terms with this and the need to get comfortable making decisions where they don’t have the in-person interaction as a crutch.

Be realistic about your target VC list (Charles’s lessons from The Brief)

- It’s really important to be honest and realistic about the list that you build when you go out to fundraise.

- A lot of the times I meet with Founders who have this dream list of investors, many of whom, given the stage, they’re at with their business, are just not appropriate.

- I think there’s a lot of wasted effort going after big-name firms to lead a seed round (for example), where for most of those firms that just isn’t their core business model.

- You might get the meeting, but I would argue that time is better spent pursuing firms whose business model is to invest in early-stage companies that have the characteristics of your business.

- A lot of Founders when they bring me their list of target firms, at least half of them are aspirational. You’ll get the meeting, but they’re not going to invest. Your time is better spent elsewhere.

Hunter Walk, Co-Founder & Partner @ Homebrew

Learn to switch deftly between pitch deck, conversation, and product demo

Homebrew has always welcomed pitches from outside of our local Silicon Valley market and has taken plenty of cold inbound emails (vs. only meeting with founders who can find a warm intro), so to be honest, the Zoom era hasn’t really changed the initial tactics used by entrepreneurs to connect with us. Additionally, we know that the last few months have thrown teams into working environments that can be random and chaotic, so a founder should never apologize if a child or pet leaps into the frame during a pitch.

My advice to founders would be to not hide behind the presentation of a deck, but rather to send materials in advance, encourage the VCs to read them (we do!), and then use the live meeting as a hybrid pitch/discussion/demo. Deftness moving back and forth between pitch deck, conversation, and a product demo takes a bit of practice. Also, if you’re going deep on a particular topic and need to convince someone of your position or explain a complex topic, you should get out of screen share slide mode, and get back to seeing faces.

It’s easier to set up meetings, but harder to observe Founders interact

Two immediate changes come to mind when considering how we’ve shifted our investment decision-making process.

- First, because there’s no expectation of meeting in-person at our office or theirs, we just jump on a call or video for a few minutes if there’s a follow-up question or chat, rather than thinking about the scheduling-lag and commitment it takes to ask someone to make a physical journey to see you again. Maybe you could say we’re scheduling in microbursts. I can imagine retaining aspects of this even when we’re all “back to normal”.

- The second area we’ve been intentional about is trying to make sure we have at least one conversation where all the cofounders are attending, which doesn’t always occur if there’s a ‘divide and conquer’ strategy going on during a particularly frenzied fundraise. Traditionally we’d all be together at some point in the process — whether for a pitch or grabbing a casual drink to talk over a term sheet or some other bonding moment. With a purely virtual investment model, you miss some of that personal interaction and as investors, we also don’t get to observe the subtle interactions between co-founders that might occur during a meal or a more relaxed setting.

So as best we can, we’ll try to get the Founders together for a virtual conversation (vs. straight-up pitch) and even sometimes do a happy hour (or morning coffee) together over Zoom as just a ‘let’s put away the deck and see if we actually enjoy being together.’ Social distanced walks can help too but we don’t want to assume everyone is comfortable with that (or isn’t also watching their kids, etc) so it’ll never be something we require.

What the perfect pitch email looks like (Hunter’s lessons from The Brief)

- People always want to know, “what does the perfect pitch email look like?”

- I want to see personality conveyed through an email. That’s kind of hard when you’re cutting and pasting the exact same message and sending it to 100 people.

- So maybe put a little bit of thought into who you’re emailing (at least that first paragraph), and why you’re interested in “Hunter at Homebrew” (for example) vs. another fund.

- Show, don’t tell: provide a link to your product, feedback from early customers or beta testers, names of people you’d hire / a stack of resumes you’ve sourced off of craigslist even ahead of having the money to hire…something that says “this already exists and I’m asking you to join my company” vs. a generic email and a generic deck that says “if you write me a check, this company might exist”. That’s a big difference.

- Try to tell me a little bit about what you’re working on, what stage you’re at.

- Please personalize it. The more information you give me, the better reaction, the more feedback I can give you.

- Whether or not it’s something I’m going to invest in, I might be able to at least make an introduction or give you another piece of data that’s going to help you tailor that pitch for the next person you talk to.

Sarah Tavel, General Partner @ Benchmark

Founders in the remote era are fundraising with more intentionality

To successfully fundraise in the remote era, if anything, it feels like founders are approaching the fundraising process with more intentionality. They are better at thinking through how to sequence the process. How to make sure they have the right introductions. Having a deck prepared.

References matter more now than ever

To me, the biggest change has been an even greater reliance on backchannel references. This is because I find it difficult to really get to know someone over Zoom. Staring at each other on a computer screen creates a formality and distance versus what you’d be able to get in the more open-ended setting of a coffee or meal together.

I miss being able to do that. I just closed a new investment in a company, and I seriously can’t wait to meet the founders in person for the first time.

What VCs are Really Looking For in a Pitch Deck (Sarah’s lessons from The Brief)

- When I was an operator, I was told about this framework: problem, solution, result. I find that to be a really great framework for understanding how to structure a pitch deck.

- I look for a clear articulation of a problem that needs to be solved, why you have the right solution (and that includes the team), and what the early results look like.

- I add a fourth category for a pitch deck, which is why you want to raise more money and what you’ll accomplish with that.

- One of the subconscious things I’m looking for in the presentation of a pitch deck is quality and clarity of thinking in the articulation of those 4 things.

- As an example, if a Founder uses a vanity metric, where they talk about something growing (downloads, MAUs, or whatever it is), and it’s not actually the metric that gets to the core of what a company’s doing, that deflates my interest.

- What I really want is someone that’s really getting to the heart of what they’re trying to do.

Mike Vernal, Partner @ Sequoia

Always be reading the room, and start the conversation early

Pre-COVID, we already routinely met with companies via Zoom, so it hasn’t been as large a change as it might seem. I think two things are even more important in a Zoom-only era.

First, you really need to read the room. In person, it’s easy to tell if you’re losing someone via their body language. If you are just talking at a set of slides on your computer, it’s much harder. Make the slides smaller and make everyone’s faces bigger.

My other piece of advice would be to start the conversation early. Our aim is to deeply partner with a few companies each year and it’s hard to build the relationship — on both sides — if you are trying to do it in a single week. Often founders get the advice to try to create urgency / FOMO and push through a financing as quickly as possible.

We can do all of the intellectual diligence quite quickly, but we think it takes time to really get to know someone and that’s doubly hard in the age of COVID. We are much more likely to lean in if we’ve had time to get to know the founder and understand the business.

In the COVID era, references are critical

We rely a lot more on references to understand what it’s like working with the team. We’ve always valued references — we can easily do 30+ references on a single company before we decide to partner — but I think they’ve become even more critical in the era of COVID.

We also encourage founders to do the same. The kinds of partnerships that we strive for often last 10-20 years. It’s important for both sides to get to know each other early and do their homework.

How to stand out to VCs as a Founder (Mike’s lessons from The Brief)

- Starting a company is an incredibly challenging process and there are a lot of ups and downs along the way, so one of the things that we really look for in Founders is grit, determination, and an implacable spirit.

- When meeting teams, understanding the adversity that the team has gone through and the way they’ve powered through that adversity is really important.

- One of the things we’re proud of at Sequoia is the number of companies we’ve backed that have been founded by first or second-generation immigrants. People who’ve come here in search of a new life and have a dogged determination to create something out of nothing that I think we really respect and admire.

Fundraising Tools for Founders:

At NFX we build software for Founders that makes fundraising faster and more transparent. These are the tools we wish existed when we were Founders. They’ve now been used by thousands of Founders and VCs to successfully get connected, get informed, and get funding.

As Founders ourselves, we respect your time. That’s why we built BriefLink, a new software tool that minimizes the upfront time of getting the VC meeting. Simply tell us about your company in 9 easy questions, and you’ll hear from us if it’s a fit.