Verticalization is no longer a growth-stage company’s game.

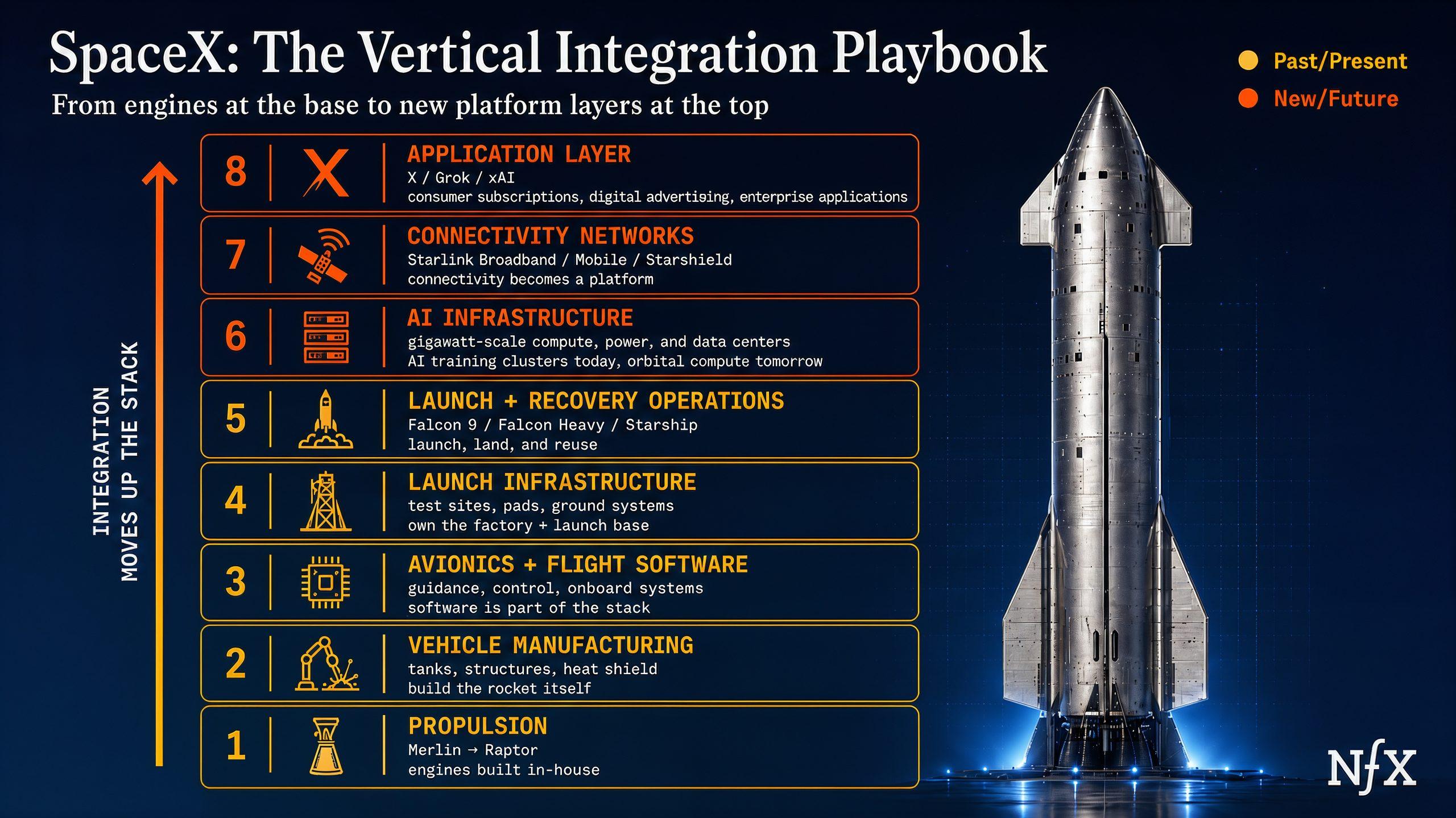

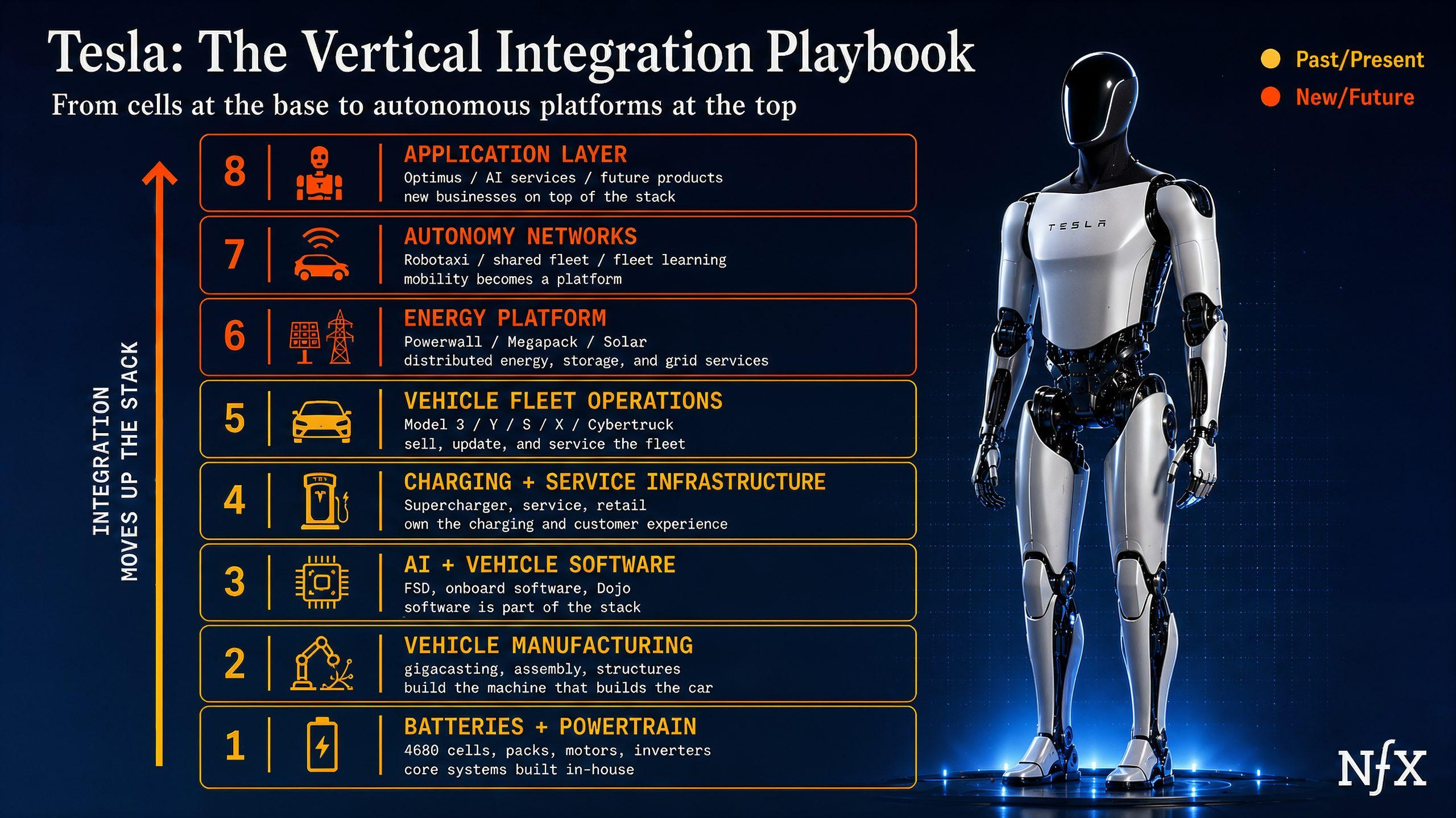

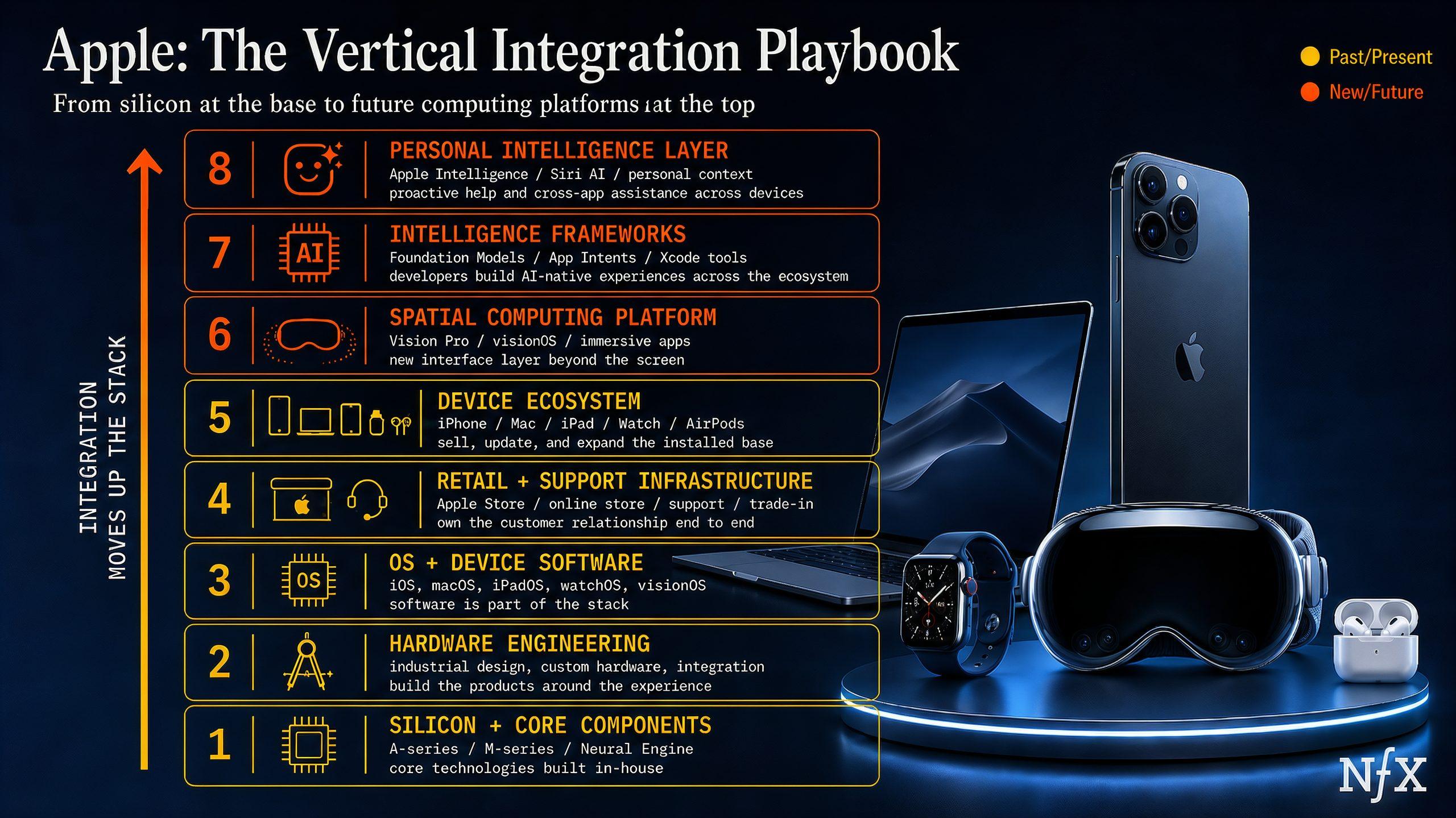

Seed-stage startups are pitching us comprehensive, vertically integrated visions. Versions of the same business plans that built Tesla and SpaceX, but adapted for high-value verticals, small teams, and AI-first thinking.

This mentality stretches across many categories: Not just AI tools for lawyers – the AI-first law firm. Not just a founder building a software procurement platform: a vision to eventually own the entire supply chain.

This mindset has always existed – it’s been Elon’s playbook for over a decade. But it’s more prominent today at earlier stages. It’s emerging because of hard lessons learned during AI’s opening act: the rise and fall of the ChatGPT wrapper company.

The companies that survived that stage (or are just building now), realize that vertical thinking is a way to stay a step ahead of the frontier labs and potentially pervasive AGI. And many are executing these visions very successfully.

Let’s talk about the shapes this strategy takes and why it’s so important today:

The Rise and Fall of the Wrapper

Vertical thinking is rapidly emerging as a defensibility in the AI era. To understand why, you have to understand what happened between 2023 and 2024.

When ChatGPT arrived, the first wave of founders did the obvious thing: they built on top of it. AI for copywriting. AI for customer service. AI for legal research. AI for sales. The pitch was always the same — take something a human does, wrap a model around it, and charge a subscription or the work that’s done.

Jasper was the poster child. It raised $125 million at a $1.5 billion valuation in 2022, and for a moment, it looked like the future of marketing software. Then, within a year, it revised its 2023 ARR forecast down by at least 30%, conducted layoffs, and watched both its co-founders step down. They’ve since re-oriented the vision around a “marketing operating system.”

Jasper was just an early, visible example of an archetype that was far more widespread. But they were not alone.

The “wrapper” companies that built single-task tools on top of foundation models had made a bet that the underlying models would stay roughly where they were.

Agents changed that thinking. The frontier labs immediately began “productizing” their models with varying degrees of success. The most obvious example here is Anthropic, which has grown its revenue run rate from a $14 billion run rate announced in January to crossing $47 billion in annualized revenue this May, largely driven by enterprise demand. You can see this in their productization strategy: Claude Code, Claude Design… all tools that would have been just wrappers two years ago.

Anyone who built their system around a single task was in trouble. The “AI for X” framing, which had seemed like a product strategy, turned out to be a description of a temporary advantage. (Side note, companies building generalist agents without network effects, or vertical expertise thinking may just be wrappers 2.0…)

What survived — and what is accelerating right now — looked different from the start. The companies that are winning today didn’t think of themselves as AI tools layered atop a model. They thought of AI as the mechanism for delivering a service — and they built toward owning the entire workflow that the service required.

EvenUp is a clear example. EvenUp began with a deep niche likely miles away from the purview of many AI labs or even “AI legal” companies: personal injury. Today, over 2,000 firms depend on its platform, including 20% of the top 100 U.S. personal injury practices, with ARR doubling year-over-year. In October 2025, the company raised a $150 million in Series E at a valuation of over $2 billion — more than doubling in under a year.

Further AI did the same for insurance. Our company Blitzy did the same for enterprise software development.

The throughline in both cases is the same: the founders were building AI as a service from day one, not AI as a feature. The real value was always in the combination of the workflow, the domain knowledge, the data that accumulated with every case or every codebase, and the understanding required to operate and sell into a high-complexity vertical. It was not in the model itself, or the data alone, or even the UX.

This is an exact inversion of the thinking that gave rise to the “wrapper generation.” Back then, the thinking was that intelligence was the selling point. The wrapper was just scaffolding. But this turned out to be false.

“The factory is the product.” This is now more true for everyone, even at the early stage.

Verticalization Strategies at Early-Stage

The companies that have survived wrapper generation have had a simple POV from the very beginning: own an entire industry (marketing, legal, enterprise coding). The workflow is the product. The data is the product. The sales pipeline is the product.

Below are some verticalization strategies we’re seeing from companies at an early stage – too early to own an entire hardware and sales pipeline perhaps (though that’s part of the long-term vision). But effective enough to develop a moat nonetheless.

Let’s dive into three we’re seeing work very well:

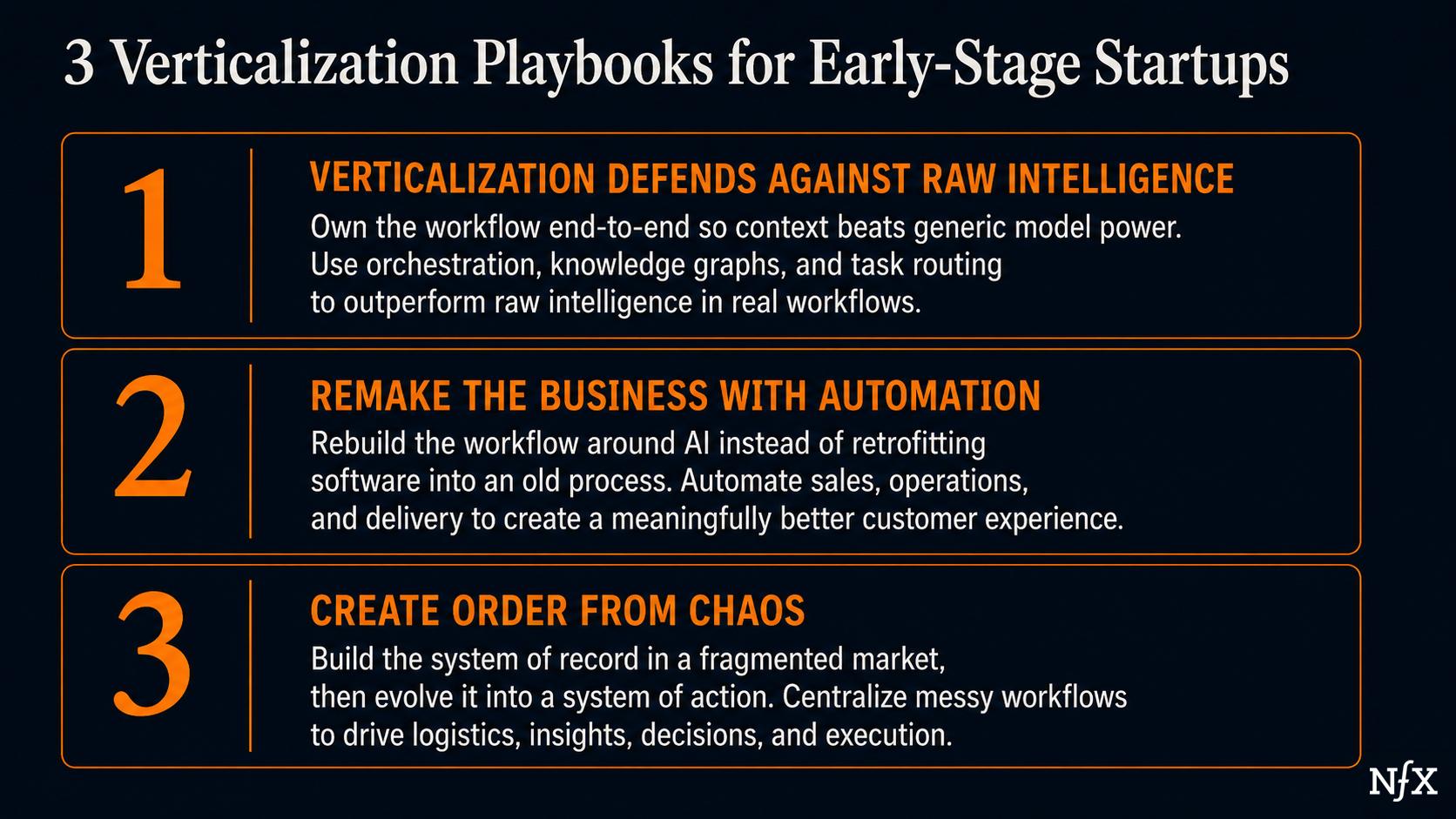

Approach 1: Verticalization Defends Against Raw Intelligence

Back in 2024, we were the first money into Blitzy – an AI platform developing custom enterprise software for the Fortune 500. Today, Blitzy’s platform outperforms Google’s, Anthropic’s, and OpenAI’s models in solving enterprise software problems. They recently raised $200M at a $1.4B valuation.

When most enterprises develop software, they rely on swarms of contractor armies. When co-founders Sid and Brian founded Blitzy, there were two ways to look at the enterprise coding market.

Option 1: sell to the contractor armies – develop a product like Cursor or Codex that they can use to better serve the market.

Option 2: Create AI so good that it would eliminate the need to hire a contractor army at all – turn the AI itself into the service and sell it to the enterprise.

They went with option 2. This was controversial at the time. Back in 2024, everyone thought that OpenAI or Claude’s models would become so powerful that no startup could compete. Raw intelligence could solve any problem.

This turned out not to be true. Blitzy’s orchestration layer – a knowledge graph of an entire company’s codebase, and the ability to break tasks into many smaller ones and query the most relevant models – performed better than the AI labs’ products in real-life enterprise contexts. Their system is so good at understanding the context around a company’s codebase that it is now #1 on SWE-Bench Pro at 66.5%.

The takeaway here is that owning a complex workflow from top to bottom, at the end of the day, beats out the raw intelligence of the frontier labs.

This is a pattern that is likely to repeat on a far larger scale as we progress toward AGI (or ASI) in the near future. Raw intelligence will “solve” many core engineering or systems problems that are bottlenecks to innovation. But that intelligence still needs to be operationalized. Vertical integration is that process, and it may prove to be a powerful defensibility in the future.

It’s already working today.

Approach 2: Remake the Business With Automation

Here’s another example: NFX-backed company Tomo, in the mortgage industry. This is a case study in why it can make sense to rethink the entire architecture of an existing product and bring automation into the center.

There are lots of companies attempting to sell software (and AI) to mortgage companies. But the bigger opportunity is rethinking the idea of how you underwrite and get a mortgage with AI at the center.

Tomo has taken that approach, using automation to “remake” the way the mortgage industry operates. They’ve applied automation across sales, underwriting, and operations. Tomo’s productivity per loan office is meaningfully higher than competitors’. And that translates to better rates for consumers. Today, 77% of homebuyers get a better rate with Tomo than with a traditional provider.

Sometimes, remaking the industry from the ground up translates to a better experience than retrofitting software into an established workflow.

Many founders miss opportunities like these because they perhaps overestimate the impact that marginal software gains can have inside a system that was never built for them. You can spend energy trying to convince people to re-make the workflow – or you can rebuild it entirely, and spend that energy making the customer’s experience better. (And as a side note, incumbents are extremely unlikely to take this approach because it requires destroying their former business model and organization.

The former strategy was very effective for the SaaS era. But AI has allowed us to move past that. It’s power allows us to rebuild traditional industries around automation. The focus now moves toward improving the customer experience rather than sweating the internal adoption of AI workflows.

Approach 3: Create Order from Chaos (Build the System of Record)

Finally, there’s a third shape to this: developing a system of record. The verticalization strategy works very well when you create order from disorder.

That’s the case with our company Seso.

We invested in them back in 2020 because they were building a system of record in HR for the American agricultural industry. At this time, this system was basically non-existent: H2-A, the visa process that powers much of American agriculture, is fragmented across law firms, Microsoft Office products, and in some cases, pen and paper.

Seso created a simple, centralized database for this process, allowing farms to finally manage their seasonal workforces the way traditional businesses manage their employees.

But then, the AI wave provided them a new opportunity: transform from a system of record into a system of action.

Seso has transformed itself from a “digital filing cabinet” into a system of action. They have re-oriented their platform (beginning with their n of 1 system of record) into an action-oriented process that can manage employee logistics, generate business insights, and even drive labor decisions.

The universal takeaways here are that if you can build a system of record, the next step is to move toward a system of action. We’ve invested in a number of other companies taking this approach like Rec in the recreation space and Veras in the long-term healthcare space.

Potential Competitive Dynamics

So far, this shape is working. But there’s a risk: a competitive dynamic between vertical incumbents powered by frontier labs and AI-native startups looking to remake the category.

Picture a big law firm that sees the “AI law firm” coming. Rather than share its in-house intelligence with a third party that could become a competitor, it partners directly with a frontier lab and takes automation in-house. This is already happening — Freshfields recently partnered with Anthropic to build customized tools.

But this play is only available to enormous players, like Big Law, major financial institutions. Even for them, partnering with the Frontier labs will be expensive – perhaps too expensive. Outrageous tokenLLM bills are starting to come due here (see examples from Uber to Microsoft) on top of expensive AI engineers. If the frontier labs and industry incumbents want to work together, the industry incumbents will have to fight the urge to gatekeep proprietary knowledge which may have limited long term value, and Frontier Labs will have to resist the urge to flex their pricing power.

Even if both parties reach an agreement, automation is still one of many functions of an industry incumbent, not the core focus.

Meanwhile, AI-native services may be more nimble. They are not beholden (too much) to the Frontier labs. They can focus entirely on GTM, and improving customer experience. Focused verticalization creates defensibility.

In the face of this dynamic, Tomo’s approach may be the model here. Even if traditional mortgage providers partner with frontier labs, Tomo’s advantage holds: a cheaper, more streamlined option for customers – one that cuts directly against incumbents’ interests.

None of this eliminates the competition. But it may contain it.

The Verticalist’s Advantage As Progress Toward AGI

The wrapper generation is dead. The survivors and the next generation of startups will think vertically. “How do I own every piece of the value chain?”

Vertical thinking is emerging as one of the few genuine defensibilities that may endure through our transition to AGI. Raw intelligence will likely unlock new, unprecedented innovation, but that innovation will still need to be operationalized and delivered to a customer.

That’s the game of verticalization.

The founders who see it early are building positions that may genuinely endure, even in the era of AI hyperscalers.

*(Note there are some oases – namely in bio and deep tech – where execution is still so specialized that it remains a moat).

As Founders ourselves, we respect your time. That’s why we built BriefLink, a new software tool that minimizes the upfront time of getting the VC meeting. Simply tell us about your company in 9 easy questions, and you’ll hear from us if it’s a fit.